Tue 24 Feb: After the Bell

Dip-Buyers Step In as Tech Bounces Back. Your 4-min takeaway →

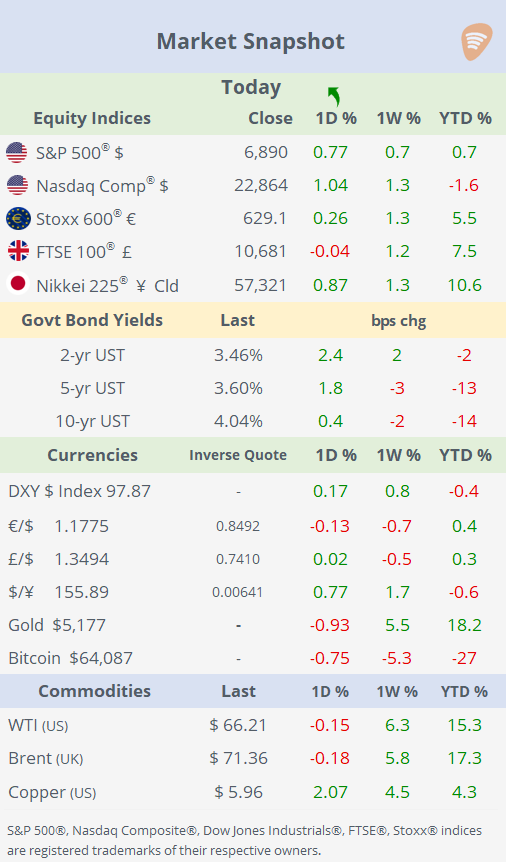

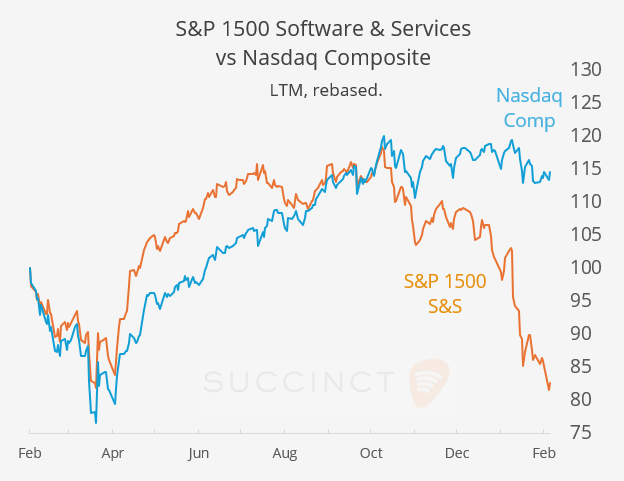

Stocks on Wall Street rebounded on Tuesday, led by a relief rally in software and broader tech names after Monday’s AI-driven sell-off, as dip-buyers stepped back in amid the absence of fresh negative headlines. Elsewhere, the dollar, gold and crude oil were little changed, while Bitcoin was volatile but ended roughly flat after briefly trading near $62,000.

Remarks by Fed officials leaned toward caution on immediate rate cuts and emphasis on data progress, interpreted by markets as relatively hawkish. Traders increased their bets for no rate change at the Fed’s next meeting (Mar 18) from 94.5% on Monday to 98% today.

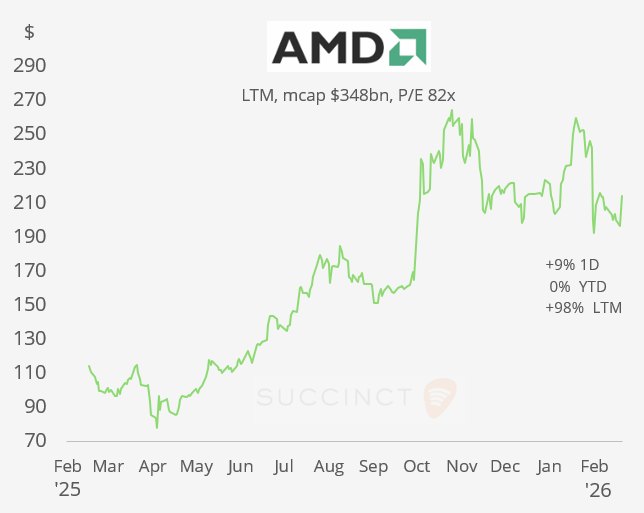

Business: → Meta Platforms struck a more than $100bn AI chips deal with Advanced Micro Devices, agreeing to buy 6GW of custom MI450 computing capacity and receiving warrants that could lift Meta’s stake to up to 10% of AMD, as the chipmaker steps up its challenge to Nvidia in large-scale AI infrastructure. AMD jumped 9% and is now 98% higher in the LTM.

→ JPMorgan CEO Jamie Dimon warned that today’s buoyant markets resemble the pre-2008 boom, cautioning that elevated asset prices, heavy leverage, and growing risk-taking, especially in private credit, suggest rising complacency and potential instability ahead.

→ Private AI company Anthropic rolled out expanded enterprise features for its Claude platform, adding department-specific and customizable plugins with deeper integration into major business software, reinforcing AI disruption fears across the software sector.

Economics: → The US ADP weekly employment change showed private employers adding an average of about 12,750 jobs for the four weeks ending Feb 7, marking the fourth straight week of accelerating gains and suggesting continued underlying labour market resilience despite being preliminary data.

→ US Consumer Confidence in February came in at 91.2, slightly above expectations and up from January, signalling a modest improvement in household sentiment, though it remains well below recent historical highs.

Earnings: → Tuesday’s main takeaway was Home Depot’s outlook. The company met expectations, and while the stock gained just 2%, management struck a cautious tone on housing, describing a still-“frozen” market with subdued turnover, selective consumer spending, and no meaningful recovery signalled in its sector outlook. HD is 12% higher YTD.

Geopolitics: → Four years into Russia’s invasion of Ukraine, Zelenskyy said Moscow has failed to achieve its war aims and urged Trump to visit Kyiv to underscore who the aggressor is as the conflict grinds on.

Politics: → Trump is set to deliver his State of the Union address to a deeply divided Congress that has largely ceded power to the White House, even as partisan tensions intensify ahead of the midterm elections in November.

Central Banks: → Today’s Fed commentary skewed mildly hawkish on near-term policy, even though some officials acknowledged the possibility of future easing later in the year:

Chicago Fed Goolsbee reiterated that further rate cuts could be appropriate later in 2026 if inflation demonstrably falls toward target, but stressed it’s too soon to cut without clear progress.

Atlanta Fed Bostic argued that structural labour dynamics mean the Fed can’t rely on rate cuts to offset rising unemployment and emphasised inflation risks, which comes off as hawkish relative to easing narratives.

Fed Governor Waller described a March rate cut as roughly a “coin flip” depending on upcoming labour data, implying no strong push for imminent easing and emphasising data-dependence rather than a clear dovish signal.

Corporate Deals: → Dallas-based CECO Environmental (mcap $2.1bn) agreed to acquire Austin-based Thermon Group Holdings (mcap $1.7bn ) in a $2.2bn cash-and-stock merger, creating a larger industrial platform focused on environmental, thermal and process-heating solutions. Ceco shares plunged 21% while Thermon’s added just 2%.

→ In private markets, 15-year-old Irish-American fintech start-up Stripe lifted its valuation to $159bn via a large employee share sale, easing IPO pressure as strong growth, profitability, and AI-driven payments demand allow the company to stay private longer. It also said it is considering an acquisition of all or parts of PayPal (mcap $44bn, +7% today).

→ In the banking sector, Citigroup (mcap $197bn) agreed to sell a further 24% stake in its Mexican retail unit Grupo Financiero Banamex for about $2.5bn, continuing its exit from consumer banking in the country. The buyers are a private investor group led by Blackstone and General Atlantic, alongside Brazil’s Banco BTG Pactual, with the deal priced at 0.85x book value. Citi shares are down 6% YTD.

Day Ahead:

Data → China FDI. Monetary Policy → Korea rate decision. Earnings → Nvidia (PM), Salesforce, TJX Companies, Synopsys, HSBC, Iberdrola, Bayer, Diageo, E.On.

See you tomorrow.

Copyright © 2026 Succinct.

All rights reserved. This publication contains proprietary content and is intended solely for the recipient’s personal use. Disclaimer: Our service is for informational purposes only and does not constitute personal financial advice.