Tue 24 Mar: After the Bell

From Oil Spike to Credit Stress: Markets Reprice Geopolitical Risk

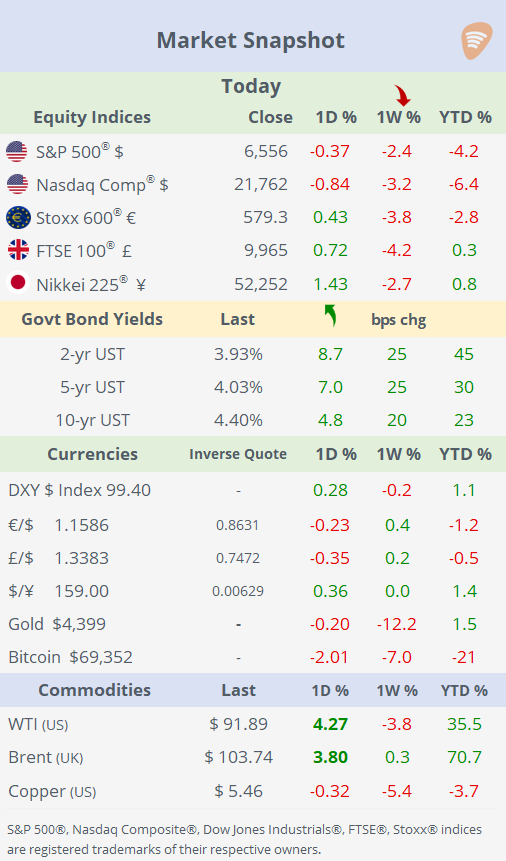

📈Today’s performance tables.

Good evening,

Risk assets are trading under pressure as geopolitical tensions re-escalate in the Middle East, with oil prices moving back above $100 following a new wave of Iranian strikes targeting Israel and Gulf countries. The conflict continues to intensify despite tentative diplomatic signals, with the Pentagon announcing the deployment of 3,000 additional troops to the region. At the same time, Iran has warned that “non-hostile vessels” transiting the Strait of Hormuz must coordinate with its authorities, raising renewed concerns over energy supply disruptions through one of the world’s most critical chokepoints. On the political front, Donald Trump indicated that the US is engaging in discussions with Iran, suggesting that both sides may be open to a deal, though markets are clearly focused on near-term escalation risks.

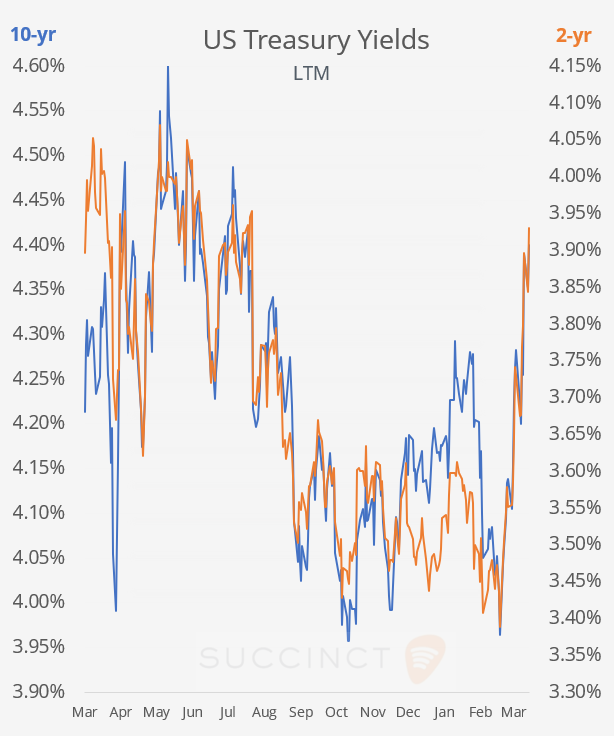

Equities are broadly lower on Tuesday while rates continue to reprice higher. US Treasury yields have risen sharply, up 25bp across the curve over the past week and ~40bp over the past month, reflecting a combination of inflation concerns driven by higher energy prices and shifting expectations around monetary policy. Notably, futures markets are now pricing in a 6% probability of a rate hike at the Fed’s April meeting, compared to 0% just a week ago, although still low in absolute terms.

At the same time, stress is building in private credit markets, where liquidity dynamics are deteriorating as investors increasingly seek to exit. Apollo has moved to limit redemptions from its Debt Solutions BDC after receiving withdrawal requests totalling $1.6bn, or 11% of net assets, more than double the fund’s 5% quarterly redemption cap. The firm ultimately fulfilled just under half of those requests. Similarly, Ares Management capped withdrawals from its $11bn Strategic Income Fund at 5%, after redemptions surged to over 11% in Q1, highlighting a broader exodus among wealthy investors from the asset class. Other large managers, including Morgan Stanley and BlackRock, have taken comparable steps to manage outflows.

Importantly, this stress in private credit has not yet transferred over into public markets. US high yield spreads, as measured by the BofA US High Yield Index, are currently at +319bp, slightly above the 12-month average but still well below the +461bp levels reached during last year’s tariffs-related volatility. This suggests that, for now, concerns around liquidity and redemption pressures remain largely contained within private markets (middle markets direct lending), with listed junk bonds showing limited signs of contagion.

Economics: → PMIs across the US, UK and €-zone showed modest softening in activity with little change vs prior months, confirming a gradual slowdown rather than a sharp deterioration, with manufacturing stabilising but services losing momentum. The surveys highlighted a clear stagflation signal, rising input costs driven by energy alongside weakening demand, but markets largely ignored the data as geopolitics and war headlines continue to dominate price action.

Corporate Deals: → Apollo will acquire Nippon Sheet Glass (mcap $305mn) in a ~$3.7bn EV deal, its largest PE investment in Japan, combining a ¥165bn ($1.05bn) equity injection with a ¥140bn debt-for-equity swap by lenders. The transaction recapitalises Nippon Sheet Glass, easing interest burden and strengthening its balance sheet to support long-term growth. Nippon shares jumped 20% on Tuesday.

→ Japan’s Sumitomo Mitsui Financial Group is reportedly preparing a potential takeover bid for Jefferies Financial Group (mcap $8.5bn), with Jefferies shares up ~3% on the news. The Japanese lender, which already holds a ~4.5% stake via Sumitomo Mitsui Banking Corporation, could act opportunistically as Jefferies stock remains ~34% lower YTD amid concerns over its private credit exposure.

→ Spanish beauty group Puig Brands (mcap €17bn) shares jumped ~13% after confirming merger talks with New York-based Estée Lauder ($26bn) over a potential tie-up that could create a $40bn+ beauty and fashion group. Both companies said discussions are ongoing with no agreement yet. Still, a combination would bring together portfolios including Charlotte Tilbury, Carolina Herrera, Tom Ford Beauty and Clinique, with over $20bn in combined annual sales. Puig shares gained 14% while Lauder’s fell 10% today.

Day Ahead:

Data → UK inflation, US imp/exp prices, current account. Earnings → Cintas, PDD Holdings, China Life.

See you tomorrow.

Copyright © 2026 Succinct.

All rights reserved. This publication contains proprietary content and is intended solely for the recipient’s personal use. Disclaimer: Our service is for informational purposes only and does not constitute personal financial advice.