Tue 27 Jan: After the Bell

Markets Extend Rally as Dollar Slides and Gold Hits New High ➡️

ℹ️ Today’s tables & charts on the ‘Market Data’ post.

Good evening,

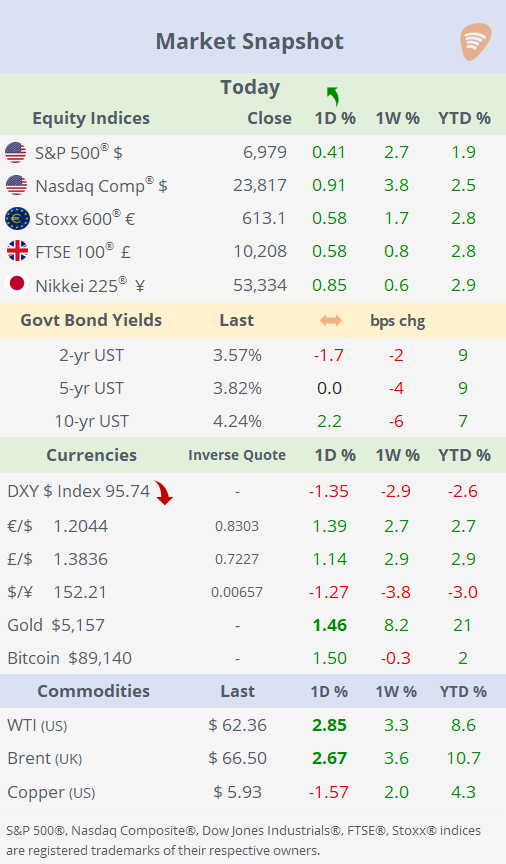

Risk assets extended their rally, with the S&P 500 reaching a fresh record after several consecutive sessions of gains, as markets looked ahead to Wednesday’s Fed decision and major mega-cap tech earnings due tomorrow. Solid corporate results, particularly from tech and consumer bellwethers, and reduced near-term geopolitical and tariff concerns continued to underpin risk appetite, even as healthcare underperformed.

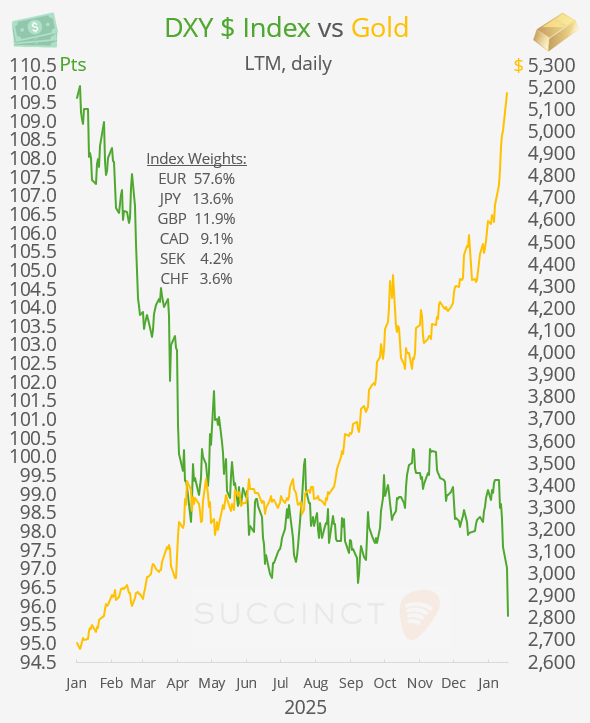

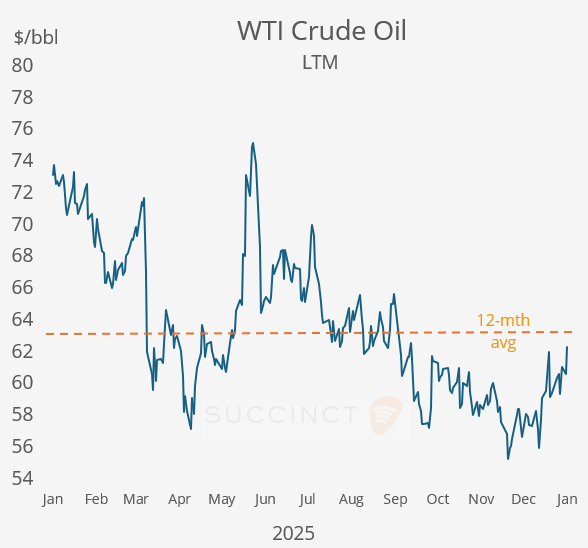

The rally unfolded alongside a sharp acceleration in the $ weakness, with the DXY index sliding ~1.3% to a four-year low as the Swiss franc, ¥, € and Aussie dollar strengthened, reflecting rising investor unease over US policymaking. Spot gold surged to a new record, up 3.3% to $5,170, while the broader precious-metals complex was mixed, and crude oil rose nearly 3% to a four-month high on US weather-related supply disruptions and lingering geopolitical risks.

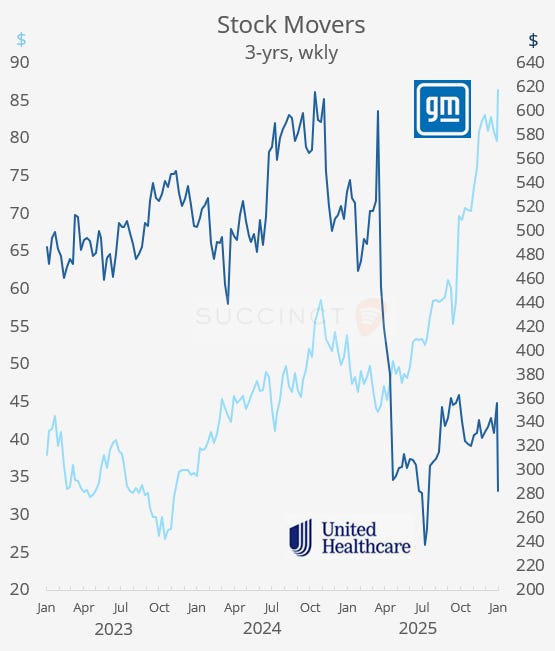

Earnings: → Today’s releases were broadly mixed, with results from UnitedHealth, Raytheon, Boeing, GM, UPS, Union Pacific and HCA Healthcare seeing varied stock responses. General Motors (mcap $83bn) surged 10% on strong Q4 results, robust guidance, a raised dividend and a large buyback program that boosted investor confidence. (CNBC)

UnitedHealth’s (mcap $255bn) shares plunged 20% after revenue came in soft, its 2026 outlook disappointed expectations and weak Medicare Advantage rate increases pressured the insurer’s future growth prospects. Other reporters saw modest moves, with UPS and HCA Healthcare edging higher on solid results, while Boeing, Raytheon and Union Pacific were largely quiet with limited stock reaction.

Business News: → US health insurers sold off sharply after Medicare proposed a 0.09% rate increase for 2027, far below expectations, triggering share declines in UnitedHealth and peers and erasing nearly $90bn in market value. (WSJ)

→ Nvidia agreed to invest $2bn in CoreWeave (camp $54bn), a cloud computing provider, to accelerate the build-out of specialised AI data centres by 2030, reinforcing its strategy of backing key customers in the AI ecosystem. CoreWeave shares jumped 11% and are 52% higher this month.

→ Amazon (mcap $2.6tn) will shut all Amazon Go and Amazon Fresh stores after failing to build a scalable economics model, converting some locations to Whole Foods as it plans to open 100+ new Whole Foods stores. Shares gained ~2.5% today. (AP)

→ UPS (mcap $91bn) plans to cut 30k jobs in 2026, extending its cost-cutting push despite higher quarterly profits, as it looks to offset soft revenues and streamline operations. (Reuters)

Economics: → US consumer confidence slumped to 84.5 in January, the lowest level since 2014 and below pandemic lows, missing expectations and raising concerns about the underlying health and uneven distribution of gains in the US economy.

→ The weekly US ADP employment data released today showed that private employers added an average of ~7,750 jobs per week for the four weeks ending Jan 3; largely a non-event for markets, as it showed stable employment trends without dramatic acceleration or slowdown and did not trigger notable market moves.

Corporate Deals: → Anta Sports (mcap $27bn), China’s largest sportswear group, agreed to acquire a 29% stake in Puma (Germany, apparel, mcap €3.5bn) from the Pinault family’s Artemis for €1.5bn, becoming Puma’s largest shareholder while staying below Germany’s mandatory takeover threshold. The deal boosts Anta’s exposure to Western markets, supports Puma’s turnaround, and pushed Puma shares up 9%.

→ In IPOs, Minnesota-based Forgent Power, an electrical equipment maker, is targeting a valuation of up to $8.8bn in a US IPO, seeking to raise $1.62bn as it taps investor demand for data-center and AI-linked infrastructure. The company plans to list on the NYSE under ticker “FPS”, positioning itself in high-growth power and energy-efficiency markets.

Day Ahead:

→ Monetary Policy Meetings: Fed (97% prob of no rate change, 3.625%-mid), Bank of Canada (unch 2.25% exp), Brazil (unch 15% exp).

→ Earnings: Microsoft, Meta, Tesla, IBM, ASML, AT&T, Starbucks.

Copyright © 2025 Succinct.

All rights reserved. This publication contains proprietary content and is intended solely for the recipient’s personal use. Disclaimer: Our service is for informational purposes only and does not constitute personal financial advice.