Tue 28 Apr: After the Bell

Equities Pull Back as AI Doubts Return

📈 Today’s performance tables.

Good evening,

Wall Street stepped back from record highs on Tuesday as a renewed wave of AI scepticism triggered a broad risk-off session ahead of a crucial stretch of Big Tech earnings. Investor sentiment was hit after reports that OpenAI (ChatGPT parent) had missed internal revenue and user targets, reviving concerns that the massive capital spending behind artificial intelligence may not deliver the blockbuster returns markets have priced in.

Technology-linked names led the pullback, with Oracle (-4%), CoreWeave (-6%) and SoftBank (-10%) among the sharpest decliners, while the major indices all finished lower. Attention now turns to results from Alphabet, Amazon, Microsoft and Meta tomorrow, followed by Apple on Thursday, a run of earnings likely to test the durability of the AI-driven rally. Elsewhere, crude oil rose again, leaving Brent up 12% on the week as supply-risk premiums remained elevated.

In commodity markets, the United Arab Emirates will leave OPEC and OPEC+ next month after nearly 60 years, saying greater independence will help it meet long-term global energy demand following recent capacity expansions. The exit is a significant blow to the cartel, removing roughly 15% of its capacity and raising questions about OPEC cohesion, while potentially aligning the UAE more closely with US calls for lower oil prices.

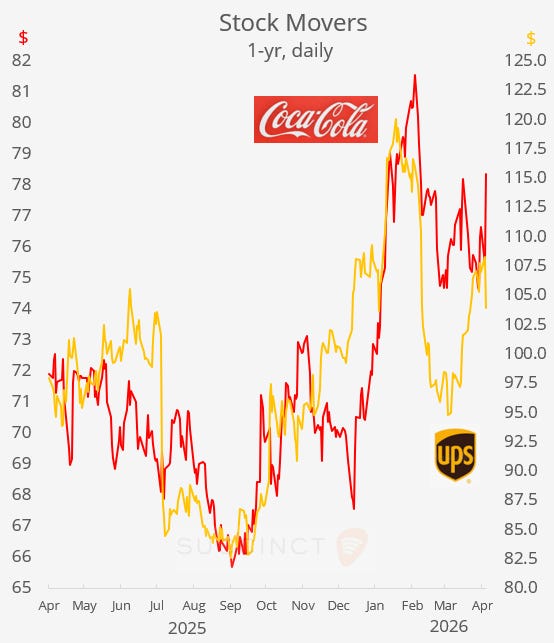

Earnings: → Most companies broadly met or beat expectations, but with few major surprises, explaining the muted market reaction across names like Visa, T-Mobile US, General Motors and Starbucks. Coca-Cola shares rose ~4% after a clear beat and upgraded full-year outlook, while United Parcel Service fell ~4% despite a profit beat due to weak US volumes and softer demand trends.

Monetary Policy: → Bank of Japan kept rates unchanged at 0.75% in a split 6-3 vote, while sharply raising its FY2026 core inflation forecast to 2.8% (from 1.9%) and cutting growth to 0.5% (from 1.0%). The BoJ flagged Middle East-driven oil price risks to incomes and profits, suggesting policy remains cautious but with some members already leaning toward further hikes.

Deals: → Private equity firm CVC is evaluating a potential €9bn take-private bid for Nexi Spa (mcap €4.5bn), whose shares have fallen sharply amid fee pressure and fintech competition. Nexi shares have lost 25% in the LTM. To ease political resistance under Italy’s golden power rules, the plan could carve out Nexi’s strategic digital banking unit for a state-backed investor such as Cassa Depositi e Prestiti.

→ German music group BMG and Nashville-based privately held label Concord will merge in a deal valuing the combined group at about $14bn, creating a scaled challenger to the music industry’s big three labels. BMG parent Bertelsmann will pay $1.16bn cash for a 67% stake, with the merged BMG headquartered in Nashville and expected to generate revenues of $2.2 bn this year.

Day Ahead:

Monetary Policy → Fed (unch at 3.75% as exp); BoC (unch at 2.25% exp); Brazil (-25bp to 14.5% exp)

Data → US housing starts, building permits, durable goods; Germany and Spain inflation.

Earnings → Mega-caps: Microsoft, Amazon, Alphabet, Meta, Qualcomm.

Copyright © 2026 Succinct.

All rights reserved. This publication contains proprietary content and is intended solely for the recipient’s personal use. Disclaimer: Our service is for informational purposes only and does not constitute personal financial advice.