Tue 3 Feb: After the Bell

Software Sector Bloodbath as Anthropic Unleashes AI Productivity Weapons ...

ℹ️Find more performance tables here. (These are not emailed).

Good evening,

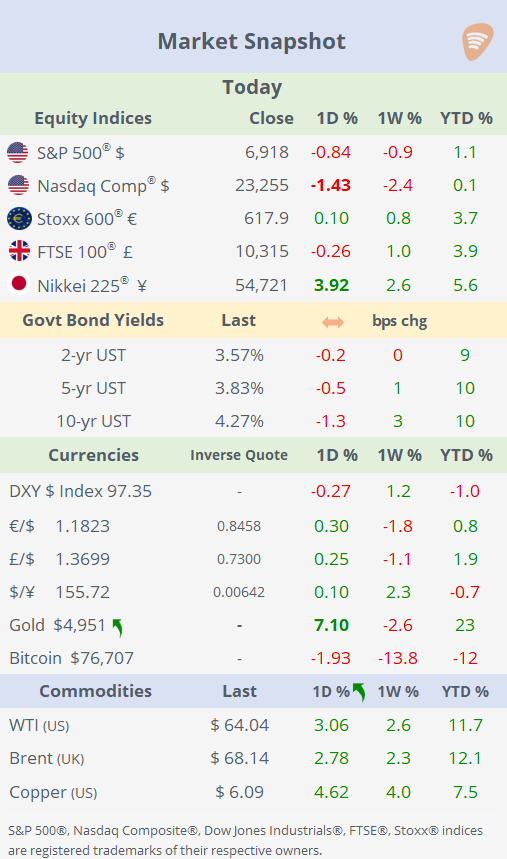

Risk assets faced a steep sell-off on Tuesday, with the Nasdaq Composite plunging as much as 2.4% intraday before partially recovering to close 1.4% lower, triggered by fresh fears of AI disruption that hammered software stocks.

Anthropic’s launch of advanced AI productivity tools slammed data services companies like Thomson Reuters, FactSet, S&P Global, and Intuit, alongside peers including Experian, Equifax, Wolters Kluwer, RELX, and even LegalZoom, Expedia. Also, big asset managers that invest in software like Ares and Apollo fell sharply. Anthropic is the San Francisco-based, privately-held AI start-up that runs the Claude models.

Volatility rippled across asset classes: gold surged 7% to near $5,000 (the biggest daily gain since 2009), silver gained 10%, crude rebounded 3%, Bitcoin fell 7% intraday before recovering to $76,500 (down 40% from the October peak).

A notable large-cap mover was Danish pharma giant, Novo Nordisk, whose ADRs plunged 14% ahead of tomorrow’s earnings on a weak 2026 sales outlook (5-13% from pricing wars, Eli Lilly competition, generics), extending LTM losses to 40%.

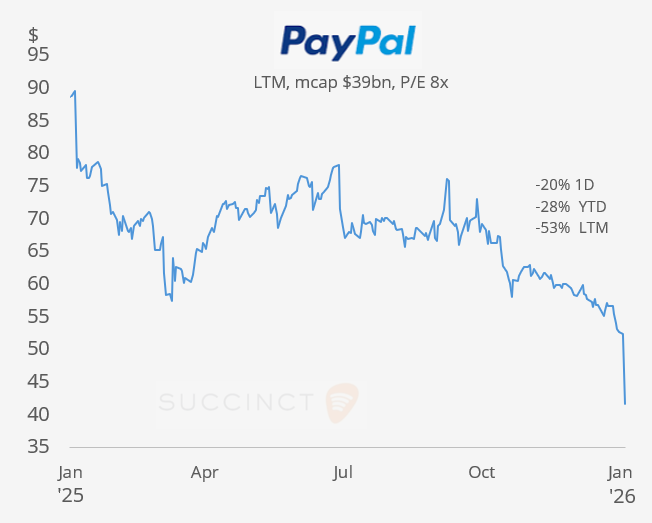

Earnings: → Were mixed today: PayPal shares plunged 20% after Q4 earnings missed top and bottom estimates ($8.7bn revenue) with weak 2026 profit guidance and a CEO transition announced. Shares are down 29% YTD and lost 53% in the LTM.

PepsiCo rallied 5% on better-than-expected Q4 profit ($2.26 EPS) from strong international demand and a $10bn share buyback pledge, while Merck climbed ~2% amid positive reception despite 2026 guidance missing estimates on Gardasil delays.

Pfizer dropped 3.5% despite Q4 revenue beat, as an in-line 2026 outlook raised patent cliff concerns. Overall sentiment is positive for consumer staples resilience, cautious on pharma growth hurdles.

Monetary Policy: → The Reserve Bank of Australia unanimously hiked rates 25bp to 3.85% today as expected, citing a material inflation pickup in late 2025 from stronger private demand and tighter capacity, forecasting trimmed mean CPI at 3.2% end-2026 before easing to 2.6% by mid-2028. The Aussie dollar rose 1% on hawkish guidance signalling possible further hikes if Q1 inflation surprises to the upside, but data-dependent outlook amid soggy growth forecasts.

Economics: → It was a quiet day on the data front. France’s January headline consumer inflation fell to +0.3% YoY (lowest since late 2020) and -0.3% MoM, driven by sharp energy disinflation and subdued demand.

Corporate Deals: → Connecticut-based Webster Financial (mcap $11.6bn) agreed to a $12.2bn takeover by Spain’s Santander (mcap €162bn), valuing Webster at $75/share, vaulting Santander into the US top-10 banks by assets with a strong Northeast presence. Webster shares jumped 9%. The deal reflects surging US regional bank consolidation amid favourable regulation, following European peers like BNP Paribas and HSBC retreating from retail. Santander also unveiled a €5bn share buyback deal ahead of tomorrow’s earnings report.

→ In private markets, Elon Musk’s SpaceX acquired xAI for $250bn (post-$20bn funding, valuing xAI at $230bn), boosting the combined valuation to $1.25tn, with SpaceX marked up to $1tn amid Starlink revenue growth. The deal unites Musk’s top ventures to develop space-based AI data centres, accelerating ambitions in the AI race.

→ Waymo, Alphabet’s self-driving car unit, secured a massive $16bn investment led by Dragoneer, DST Global, and Sequoia Capital at a $126bn valuation. The capital will expand its robotaxi fleet, enter 20 additional US cities, and launch in international markets like London and Tokyo.

Day Ahead: Data → US ADP employment change, ISM Services PMI; €-zone and Italy inflation. Earnings → Alphabet, Eli Lilly, AbbVie, Novo Nordisk, Uber, Qualcomm, MUFG, Santander, GSK.

See you tomorrow.

Copyright © 2025 Succinct.

All rights reserved. This publication contains proprietary content and is intended solely for the recipient’s personal use. Disclaimer: Our service is for informational purposes only and does not constitute personal financial advice.