Tue 3 Mar: After the Bell

Energy Shock Returns as Middle East Conflict Rattles Global Markets

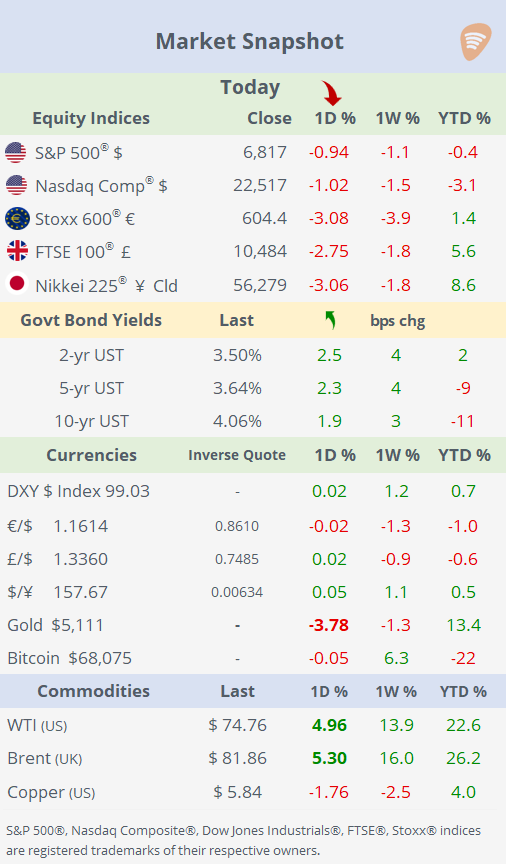

ℹ️Today’s Performance tables.

Good evening,

The conflict in the Middle East escalated sharply, triggering a significant selloff in risk assets, with missile and drone attacks spreading across the region, disrupting air travel and drawing in Gulf states as embassies, airports and energy infrastructure were hit. Iranian strikes on energy assets marked a major escalation, forcing QatarEnergy to halt LNG production and Saudi Arabia to shut key oil facilities, triggering the largest surge in global gas prices since 2022 and reigniting fears of a broader energy shock.

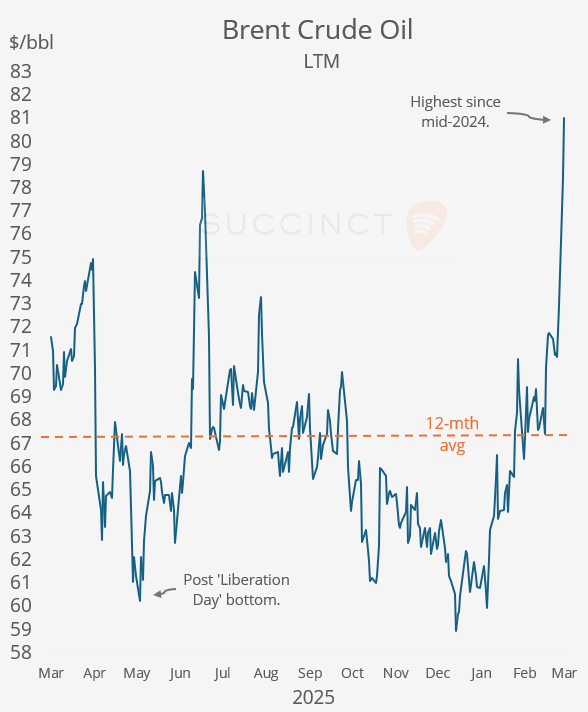

European and Asian gas benchmarks jumped up to 50%, while Brent crude briefly spiked as much as 13%, reflecting growing risks to supply routes, including the Strait of Hormuz, which Iran has threatened to target. Washington said Iran’s military capabilities have been largely neutralised and signalled it could escort tankers through Hormuz, as Israel expanded operations against Hezbollah in Lebanon and warned of further regional retaliation if attacks continue.

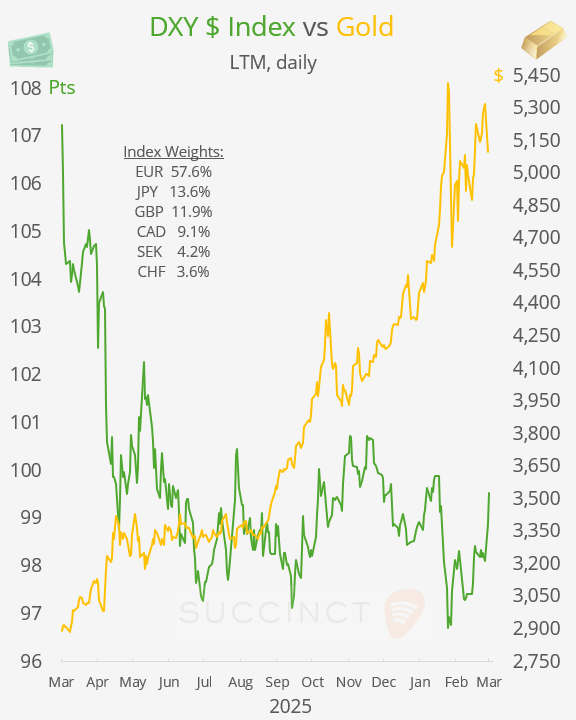

Precious metals sold off sharply as the oil-driven inflation shock pushed real yields and the $ higher, leading markets to reprice rate expectations toward fewer cuts or a high-for-longer scenario, overwhelming gold’s safe-haven appeal. Gold fell ~4%, silver 6%, and platinum 9% on Tuesday, with profit-taking and forced selling amplifying the move after a strong pre-selloff rally.

The UK, France and Germany signalled readiness to support defensive measures and reinforce regional security in response to Iranian attacks, with France deploying an aircraft carrier to the Mediterranean and European allies moving military assets to Cyprus, while Brussels continues diplomatic engagement to reduce tensions.

In private credit markets, Blackstone’s flagship private credit fund (Bcred) saw $1.7bn of net redemptions, with withdrawals reaching 8% of assets, testing the resilience of semi-liquid private credit structures. The outflows, alongside sector writedowns and halted redemptions elsewhere, have heightened investor unease and pressured listed alternative managers’ shares. Additionally, Apollo’s CEO, Marc Rowan, warned that higher rates and tighter liquidity are likely to trigger a shakeout across private markets, exposing weaker capital structures and business models. The effective yield of BofA’s US High Yield Index (listed bonds) stands at 6.7% (303bp spread).

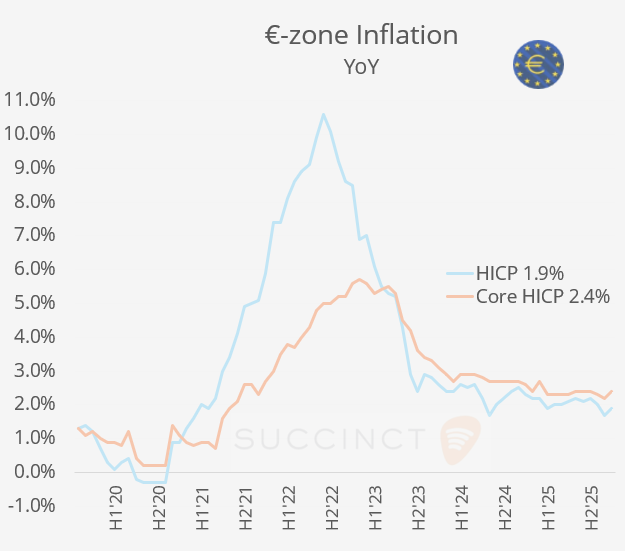

Economics: → €-zone consumer inflation unexpectedly rose to 1.9% YoY in February (vs 1.7% expected), +0.2% MoM, while core CPI climbed to 2.4% YoY (0.2% MoM), both above estimates. The upside surprise was partly driven by energy prices, with Middle East tensions already feeding through, while services inflation remained sticky at 3.4% YoY. Markets reassessed policy risk: rate-hike odds by year-end moved to ~50/50, pushing short-dated yields higher (Schatz at 2.13%) as the ECB signalled heightened vigilance amid rising inflation uncertainty.

Corporate Deals: → In the logistics & supply chain sector, Thoma Bravo will acquire privately owned WWEX Group and merge it with portfolio company Auctane, creating a combined logistics and shipping technology platform valued at up to $12bn. WWEX reported annual systemwide revenue of about $5bn last year and has a sales force of over 2,300 employees.

→ Elliott has invested $1bn in Pinterest (mcap $13bn) via convertible senior notes (30% conversion premium), with the proceeds used to fund $1bn in accelerated buybacks. The investment supports a newly approved $3.5bn share-repurchase programme, underscoring activist backing for capital returns. Pinterest shares rose 10% today but remain 26% lower this year.

→ In private markets, Paris-based Banijay Group will merge its entertainment arm with All3Media in a $5bn deal, creating the world’s largest independent entertainment producer. RedBird IMI will retain 50% of the combined group and pay €625m to Banijay. The deal will house brands such as “Peaky Blinders,” “Big Brother”, and “The Traitors” under one roof.

→ In the advertising sector, Ziff Davis (mcap $1.7bn) agreed to sell its connectivity division, including Ookla (Speedtest, Ekahau), to Accenture for $1.2bn in cash. The unit generated $231m in revenue last year, with proceeds earmarked for general corporate purposes and for Accenture to strengthen its end-to-end network intelligence offering. Ziff shares jumped over 50% today.

→ In IPO’s, PayPay, backed by SoftBank, is targeting a valuation of up to $13.4bn in a US listing, seeking to raise as much as $1.1bn despite volatile markets. The fintech has secured cornerstone investors, with analysts flagging limited near-term AI disruption risk to its payments-led business model.

Day Ahead:

Data → US ADP weekly employment change; €-zone PPI inflation; Services PMIs for the US, €-zone, UK, Spain, Italy.

Earnings → Broadcom (PM), Bayer, Adidas, Continental.

See you tomorrow.

Copyright © 2026 Succinct.

All rights reserved. This publication contains proprietary content and is intended solely for the recipient’s personal use. Disclaimer: Our service is for informational purposes only and does not constitute personal financial advice.