Tue 31 Mar: After the Bell

Markets Rally on Hopes of Imminent War De-Escalation

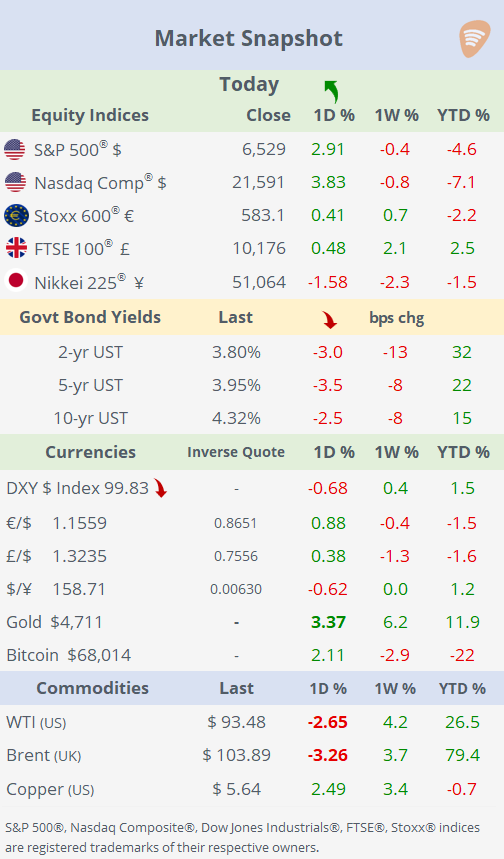

📈 Today’s performance tables.

Good evening,

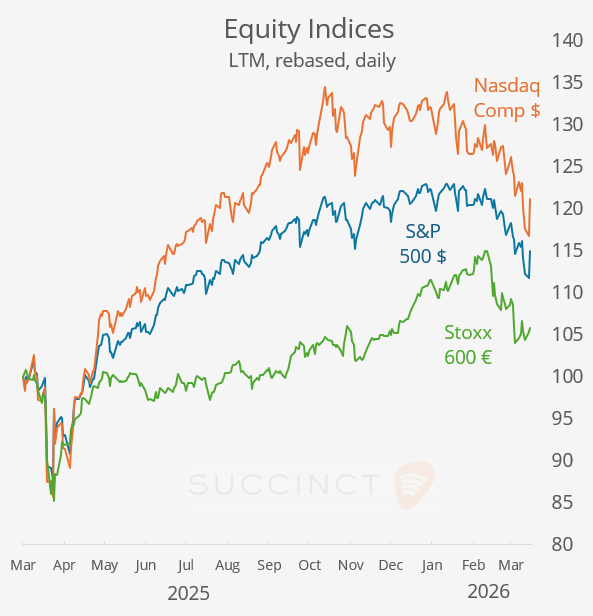

Risk assets staged a sharp reversal into risk-on mode, with equities and bonds rallying strongly as geopolitical tensions showed signs of easing. The shift in sentiment was driven by signals from Tehran indicating openness to negotiations, alongside comments from Trump suggesting the conflict may not last much longer and that Iran has been “essentially decimated”. Additional support came from US defence officials who noted a marked decline in Iranian projectile activity, reinforcing the narrative that the conflict may be approaching a turning point.

Markets reacted decisively: oil prices fell, with Brent crude down 3.2% on the day, while equities posted a strong comeback. Safe-haven and alternative assets were mixed, with gold, silver, and cryptos firmer, reflecting residual uncertainty even as broader risk appetite improved. The tone across markets was one of relief rather than full conviction, with positioning adjusting rapidly to a potentially shorter conflict horizon.

Despite today’s pullback, the energy backdrop remains extremely tight. Brent crude is still up ~70% this quarter, marking its largest quarterly gain since the 1991 Gulf War. In the US, gasoline prices have surpassed $4 per gallon for the first time since Aug 2022, while European officials continue to warn of ongoing supply disruptions, urging conservation amid the risk of prolonged stress in global energy markets.

The key near-term focus is whether diplomatic signals translate into tangible de-escalation. While markets are increasingly pricing a potential endgame scenario, policymakers caution that the coming days will be decisive, leaving a gap between improving sentiment and still-fragile fundamentals in energy and geopolitics.

Business News: → OpenAI, the creator of ChatGPT, raised $122bn mainly from Amazon, Nvidia and Softbank at an $852bn post-money valuation. Its previous round was a year ago when it raised $40bn at $300bn.

→ French AI start-up Mistral, which develops frontier AI models, raised $830mn in debt to fund Nvidia-powered data centres across Europe, amid growing demand for sovereign AI alternatives to US tech giants. The move reflects a broader trend of heavy debt-funded AI infrastructure build-out, despite rising concerns over uncertain returns and potential oversupply. The financing was arranged mostly by BNP, Credit Agricole, HSBC and MUFG as private loan.

Economics: → €-zone inflation rose to 2.5% YoY from 1.9% a month earlier, while core inflation eased slightly and came in below expectations, signaling limited underlying price pressure. The increase was primarily driven by energy prices, while underlying inflation remained contained, implying limited immediate pressure on the ECB, though second-round effects into core remain a key risk.

→ Canada GDP was slightly better than expected but still weak, reinforcing a soft growth backdrop.

→ US JOLTs job openings showed further labor market cooling (below estimates), not a shock but directionally negative.

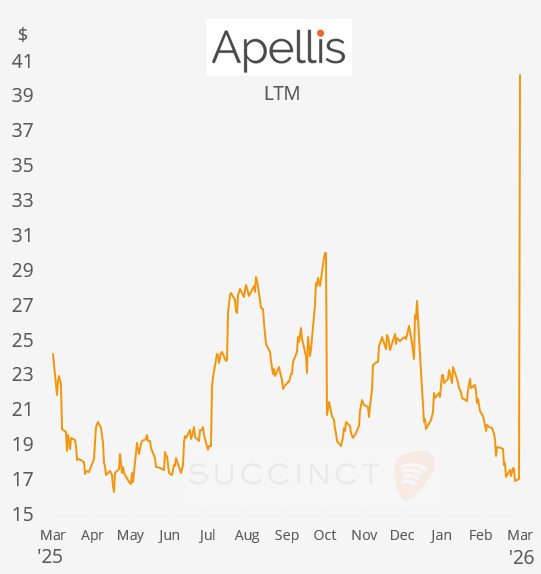

Deals: → In the biotech industry, Biogen (mcap $26bn) will acquire Apellis Pharmaceuticals (mcap $5bn), a commercial-stage biopharma mainly targeting rare diseases and ophthalmology, for $5.6bn, paying $41/share in cash plus a Contingent Value Right tied to Syfovre sales. The deal strengthens Biogen’s immunology and rare-disease pipeline, adding Syfovre and Empaveli (~$689m combined 2025 sales). Apellis shares more than doubled today.

→ Eli Lilly & Co (mcap $820bn) will acquire UK-based Centessa Pharmaceuticals Plc (mcap $5.8bn) in a deal worth up to $7.8bn, as it expands beyond metabolic drugs into sleep disorders. The acquisition centers on orexin-targeting therapies, with lead drug cleminorexton in mid-stage trials for narcolepsy and idiopathic hypersomnia, though the modest premium may invite competing bids. Centessa shares jumped 45% on Nasdaq today and are 174% higher the the LTM.

→ Unilever will combine its food division with McCormick & Co (mcap $13bn) in a $66bn deal, creating a global food group with $20bn in revenues and a 65/35 ownership split. Unilever will receive $15.7bn in cash to fund buybacks and pivot toward beauty/personal care, while initial market reaction was negative with both stocks declining. McCormick’s shares fell 6% and are 26% lower YTD.

Day Ahead:

Data → US ISM Manufacturing PMI, retail sales; Korea and Indonesia inflation; Switzerland retail sales. Earnings → n/a.

See you tomorrow.

Copyright © 2026 Succinct.

All rights reserved. This publication contains proprietary content and is intended solely for the recipient’s personal use. Disclaimer: Our service is for informational purposes only and does not constitute personal financial advice.