Tue 7 Apr: After the Bell

Ultimatum Countdown: Markets Brace for US–Iran Showdown at 8pm ET

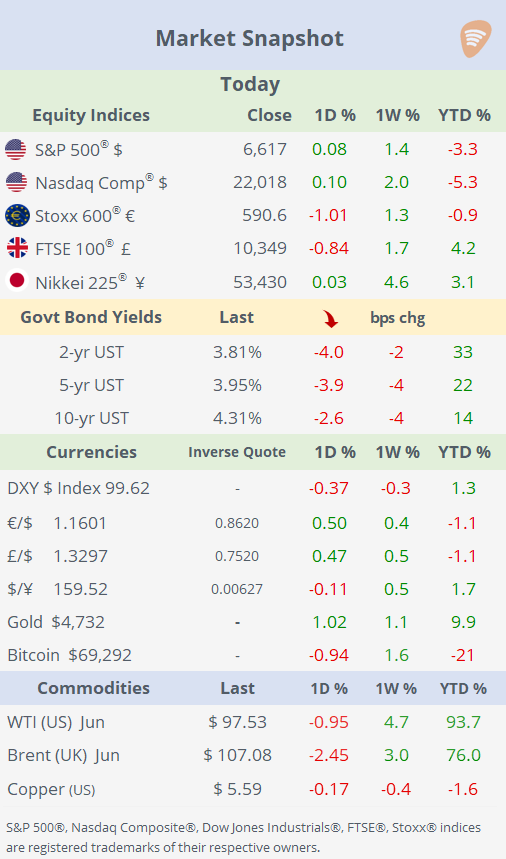

📈 Today’s performance tables.

A sharp escalation in the US–Iran conflict has dominated market narrative and price action over the past 24 hours, driving significant intraday volatility across asset classes. Tensions intensified after Trump issued a stark ultimatum, setting an 8 pm ET Tuesday deadline for a ceasefire agreement tied to reopening the Strait of Hormuz, a critical artery for global oil flows.

The rhetoric marked a notable step-up in geopolitical risk as Trump warned:

“A whole civilisation will die tonight, never to be brought back again. I don’t want that to happen, but it probably will”

while reiterating threats to target Iran’s infrastructure, including power plants and bridges, if no agreement is reached.

Behind the scenes, mediators, including Pakistan, are pushing for a two-week pause, although Iran has reportedly stepped back from negotiations following the latest escalation. Meanwhile, US strikes on Kharg Island, one of Iran’s key oil export hubs in the Persian Gulf, underscore the growing risk of supply disruption beyond the Strait itself.

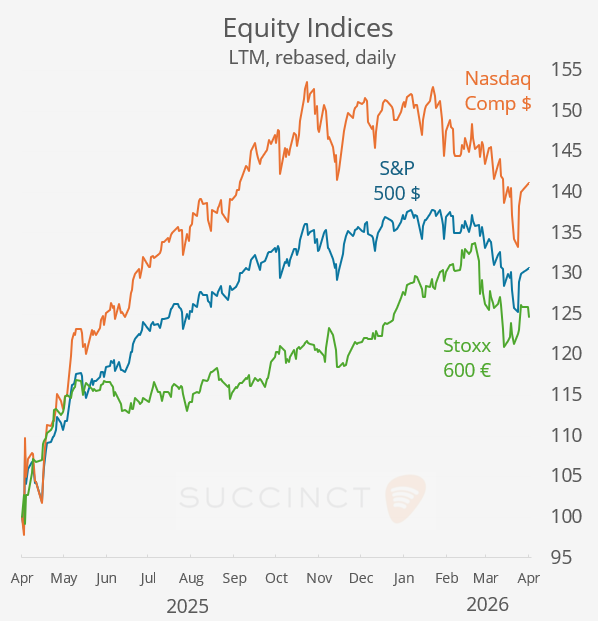

Markets reflected this binary backdrop. The S&P 500 initially dropped over 1% before recovering into the close, finishing broadly flat as investors positioned for a potential last-minute diplomatic resolution. Price action suggests markets are assigning some probability to de-escalation, despite the increasingly aggressive rhetoric.

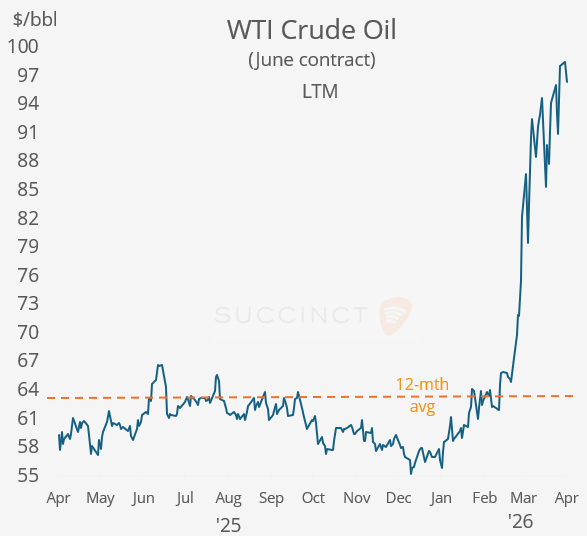

Front-month (May) WTI crude surged more than 5% intraday to $117, its highest level since mid-2022, before reversing to end slightly lower, highlighting the extreme sensitivity to headline risk. The session encapsulated the current regime: sharp, headline-driven swings with positioning anchored around a binary geopolitical outcome.

Stepping back from the immediate geopolitical noise, a broader structural theme in equities remains firmly in place: the S&P 500 dividend yield has fallen to ~1.25%, near 50-year lows, despite dividends historically contributing approx 30% of long-term returns. This reflects index concentration in low-dividend Big Tech, such as Microsoft and Nvidia, which favour reinvestment and buybacks over cash payouts.

Economics: → US durable goods orders fell -1.4% MoM in February (vs -0.5% expected), dragged by a pullback in aircraft, while core capital goods remained more resilient, pointing to underlying business investment holding up.

→ US ADP employment change averaged +26,000 (4-week average), marking the third consecutive week of improvement and the strongest pace since the series began, pointing to a rebound in hiring momentum. While the level remains modest in absolute terms, the steady acceleration suggests labour market conditions are stabilising after recent softness, reinforcing a cautiously positive near-term outlook.

Deals: → Private equity buyout activity slowed sharply in Q1’26, with deal value falling to $170bn (-36% QoQ, -8% YoY) as geopolitical tensions and uncertainty around AI’s impact on tech weighed on dealmaking. The sector continues to face headwinds from higher rates and difficult exits, while fundraising remained relatively resilient at $86bn.

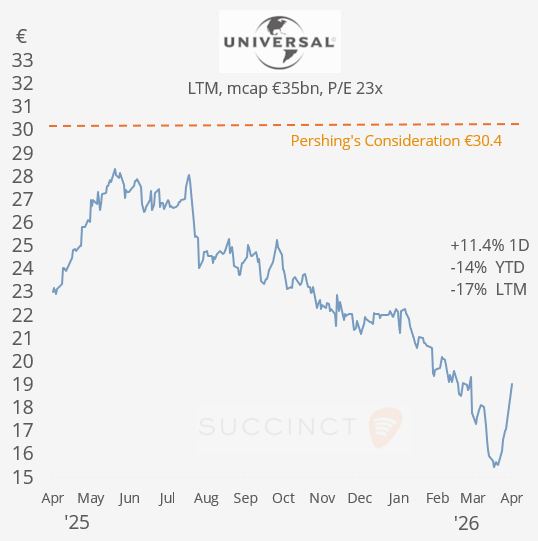

→ New York-based Pershing Square Capital Mgt, led by Bill Ackman, is bidding for Netherlands-based Universal Music Group (mcap €35bn) in a ~$60bn deal via a merger with its SPARC (Special Purpose Acquisition Rights Co) vehicle, aiming to relist the group on the NYSE. The proposal targets UMG’s perceived valuation discount despite strong fundamentals, with the transaction expected to close by year-end if approved. UMH shares in Amsterdam gained 11% today but remain 17% lower in the LTM.

→ California-based biotech Gilead Sciences (mcap $172bn) will acquire Germany-based Tubulis for $5bn, expanding its oncology pipeline with next-generation antibody-drug conjugates (ADCs). The deal strengthens Gilead’s position in targeted cancer therapies, adding early-stage assets built on Tubulis’ proprietary ADC platform. Tubulis is a private, venture-backed biotech, owned by a syndicate of VC and institutional investors (e.g. Venrock, EQT Life Sciences, Nextech Invest, Wellington, etc.), alongside founders and management.

→ Blackstone and NY-based investment firm Tinicum will acquire aerospace & defence Senior Plc (mcap £1.2bn) of the UK for £1.4bn in cash, marking another takeover of a London-listed industrial company. Senior shares gained 50% YTD.

Day Ahead:

Data → US FOMC Minutes, €-zone retail sales, Germany factory orders.

Monetary Policy → India (unch at 5.25% exp)

Earnings → Delta Air Lines (PM).

Copyright © 2026 Succinct.

All rights reserved. This publication contains proprietary content and is intended solely for the recipient’s personal use. Disclaimer: Our service is for informational purposes only and does not constitute personal financial advice.