Tue 7 Oct: After the Bell

🎙️📄+ Market Data

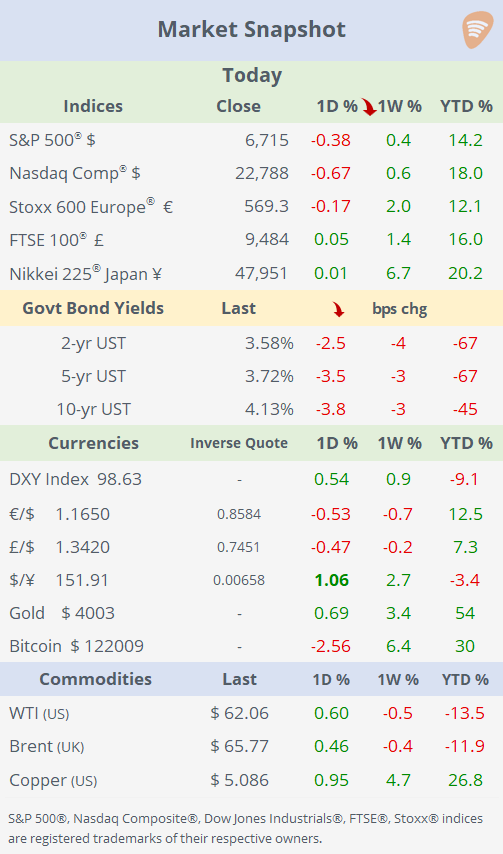

See the ‘Market Data’ post for tables & charts.

Good evening,

US equity indices pulled back from record highs, driven by profit-taking ahead of the Q3 earnings season and investor concerns over AI valuations. All benchmarks fell on Tuesday, with mid and small-cap indices as the underperformers, dropping over 1%. The consumer discretionary sector was the day’s biggest loser, impacted by Tesla’s 4.5% drop following the introduction of more affordable models. Markets are still awaiting September’s Non-Farm Payrolls report, which has been delayed due to the government shutdown.

Cryptos also retreated from their peaks, with Bitcoin trading at $122,000 after hitting an all-time high of $126,300 earlier in the week. The DXY $ index rose 0.5% to its highest close in two months, bolstered by a weakening ¥ and declines in the € and £.

Gold futures (Dec) surged past $4,000 for the first time, as investors turned to alternative assets amid concerns over the dollar, interest rates, and global financial stability. Its 50% gain in 2025 has outpaced rallies during the GFC and the pandemic, marking the largest annual jump since 1979. Political pressure on the Fed to cut rates has further fueled demand for gold as a safe-haven store of value.

Central Banks: Fed Governor Miran said today that the relative calm in bond markets bolsters the case for a faster reduction in interest rates. He also expressed disappointment that the FOMC did not deliver more aggressive cuts at its last meeting. Markets continue to price in an almost certain quarter-point rate cut by the Fed on Oct 29, bringing the target range to 3.75% - 4.0%.

Data: Germany’s factory orders fell 0.8% MoM in August, significantly missing expectations of a 1.1% increase. This marks the fourth consecutive monthly decline. However, on an annual basis, factory orders rose by 1.5%, a steep improvement from the previous month.

Business: Tesla unveiled more affordable versions of its Model 3 and Model Y, priced below $40k. These stripped-down models lack features like Autosteer and rear touchscreens, and the price cuts do not fully offset the loss federal EV tax credit that expired in September. Tesla’s stock fell 4.5%, reflecting investor concerns that the new models may not sufficiently boost demand or differentiate Tesla from increasing competition in the EV market.

Debt Markets: JPMorgan analysts say there is now $1.2tn of high-grade debt linked to AI businesses, more than the exposure to U.S. banks, as AI-driven corporations take up a 14% share of the investment-grade bond market. That marks a significant shift in credit markets, reflecting surging investor appetite for AI exposure through debt instruments rather than just equity (see Market Data for Index chart).

Deals: In private markets, the Intercontinental Exchange (mcap $92bn), parent of the NYSE, plans to invest up to $2bn in Polymarket, the crypto-based prediction platform known for its real-time wagering on global events. The move marks ICE’s boldest step yet into decentralised finance, with the firm seeking to formalise oversight of a market long operating outside U.S. regulation.

IPOs: California-based biotech MapLight Therapeutics is aiming to raise $262mn from its listing on Nasdaq, with the proceeds earmarked for its challenger to Bristol Myers Squibb’s schizophrenia med Cobenfy.

Day Ahead: FOMC Minutes and Germany industrial production. (No significant earnings releases or monetary policy decisions scheduled)

See you tomorrow.

Copyright © 2025 Succinct.

All rights reserved. This publication contains proprietary content and is intended solely for the recipient’s personal use. Disclaimer: Our service is for informational purposes only and does not constitute personal financial advice.