US Regional Banks Face Turbulence Amid Loan Failures

Context & Background in 3 minutes⌛

This week’s spotlight fell on regional banks, as mounting credit losses and recent private company bankruptcies revived concerns over lending standards and exposure to private credit.

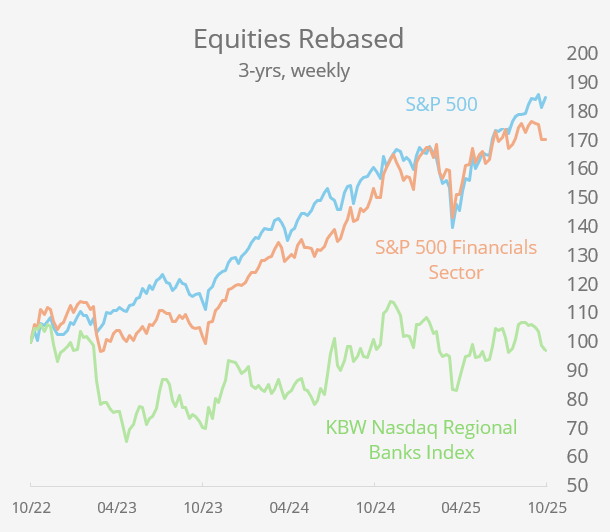

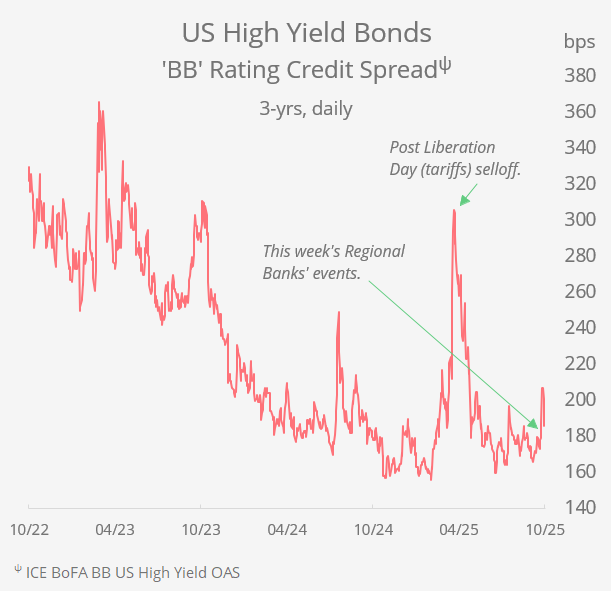

US regional banking stocks fell sharply on Thursday, rattling investors and reigniting concerns about credit quality in the broader market. Shares of Zions Bancorp (mcap $7.3bn) dropped over 13% (-8% YTD) after the bank announced a $50mn charge-off on two troubled loans issued through a subsidiary. Western Alliance Bancorp (mcap $8bn) similarly revealed exposure to a fraudulent borrower, sending its stock down 10% (-13% YTD). Even Jefferies Financial Group (mcap $11bn), a Wall Street investment bank, fell ~9% (-34% YTD) as worries over off-balance-sheet lending and shadow banking practices amplified caution among investors.

The recent turmoil can be traced to a series of high-profile collapses in the US automotive sector. First Brands, an Ohio-based auto parts supplier, filed for Chapter 11Ψ bankruptcy in late September. Its filings disclosed liabilities ranging from $10 to $50bn against assets of just $1-10bn, much of it stemming from opaque off-balance-sheet financing. In a dramatic emergency court filing, First Brands’ creditors claimed that $2.3bn in assets had “simply vanished.” Among the lenders with significant exposure were Jefferies, which reported $715mn in loans to the company through a controlled asset manager, and UBS, which also holds hundreds of millions in claims.

First Brands’ founder, Malaysian-born businessman Patrick James, built the company through an aggressive debt-fueled acquisition spree, buying 24 automotive-related businesses, including Trico, a windshield wiper manufacturer. Renamed First Brands Group in 2020, the firm’s rapid expansion relied heavily on non-traditional financing channels. The bankruptcy underscores how risky lending practices, particularly those outside conventional banking oversight, can quickly cascade into broader market anxieties.

Earlier in September, the collapse of Tricolor Holdings, a Texas-based subprime auto lender and used car retailer, set off initial waves of concern for regional banks. Tricolor Auto, which specialised in car loans to low-income borrowers, filed for Chapter 7Ψ bankruptcy amid allegations of fraudulent activity. Thousands of borrowers were left stranded, and Fifth Third Bancorp (mcap $27bn) disclosed potential losses of around $200mn. These failures illuminate the growing reach and potential hazards of private credit, financing that operates outside the regulated banking system.

Private credit, often referred to as part of the “shadow banking” sector, has expanded rapidly since the GFC. It’s a broad asset class that includes a range of investment strategies such as direct lending, mezzanine and distressed debt, asset-backed finance, real estate, and infrastructure. Some of these may involve unsecured corporate loans. Dominated by alternative asset managers like Blackstone, Apollo, Ares, and KKR, the sector now manages ~$2.5tn in assets globally. Though still a fraction of the $190tn in total banking assets worldwide, private credit’s influence is significant because it is far less constrained by regulatory capital requirements or disclosure obligations. This flexibility allows non-bank lenders to issue loans faster and to a wider range of borrowers than traditional banks, but may also create systemic risks that are less visible to regulators.

The confluence of these events has highlighted the vulnerabilities of US regional banks, which often have concentrated exposure to local industries and commercial borrowers. Zions and Western Alliance are not alone in facing potential losses from opaque lending practices. The collapse of First Brands and Tricolor illustrates how troubles in private credit can reverberate through the traditional banking sector, raising broader questions about underwriting standards and risk management. Analysts note that while private credit offers high yields and growth opportunities, its lack of transparency and limited oversight could make future shocks even more acute.

In the weeks ahead, investors will be watching how regional banks manage their exposure to non-traditional lending and whether regulators increase scrutiny of private credit channels. For now, the lesson from this week is clear: even as US regional banks appear resilient, the combination of fraudulent activity, leveraged borrowers, and shadow banking connections creates vulnerabilities that can spread quickly through financial markets.

Largest Regional Banks: The PNC Financial (mcap $70bn), U.S. Bancorp ($72bn), Truist Financial ($54bn), M&T Bank Corp ($28bn), Fifth Third Bancorp ($27bn).

Mid-sized Banks (links to Morningstar’s Key Metrics): Zions Bancorp, Western Alliance Bancorp, First Horizon Corp, Huntington Bancshares and KeyCorp.

ΨChapter 11 bankruptcy allows a company to restructure its debts and continue operating, giving it time to negotiate with creditors while staying in business.

Chapter 7 bankruptcy involves the liquidation of assets, where a company ceases operations and sells off assets to repay creditors as much as possible.

Copyright © 2025 Succinct.

All rights reserved. This publication contains proprietary content and is intended solely for the recipient’s personal use. Disclaimer: Our service is for informational purposes only and does not constitute personal financial advice.