Wed 1 Apr: After the Bell

Hormuz Hope Rally Gains Momentum; Trump Addresses Nation Tonight

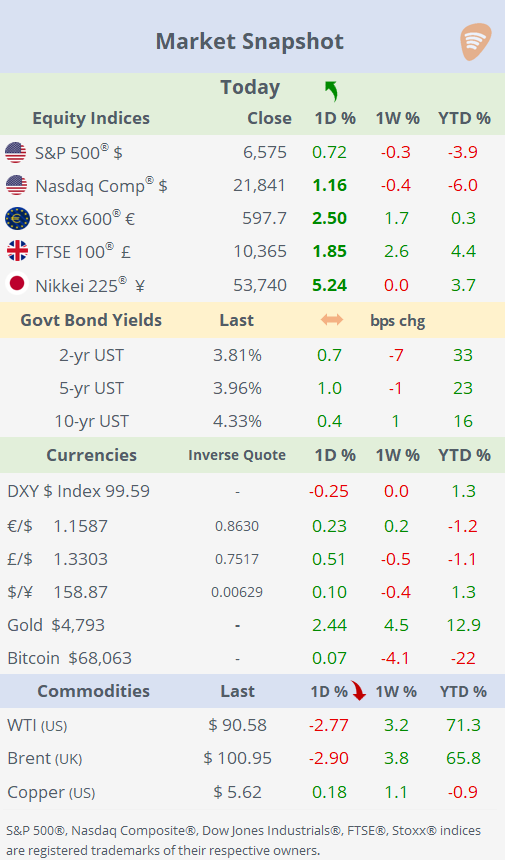

📈 Today’s performance tables.

Good evening,

Global markets extended their risk-on rebound, with equities rallying for a second consecutive session on growing optimism that the conflict with Iran may be nearing an end. The so-called “Hormuz Hope” rally gained traction as oil prices continued to decline, reflecting easing fears around supply disruptions despite the Strait of Hormuz remaining largely constrained. Sentiment was further supported by comments from Iran’s president, Pezeshkian, signalling openness to de-escalation, alongside expectations that Trump will outline a potential timeline for ending the war in a rare primetime address later tonight (at 9 PM ET).

The positive tone was broad-based across regions. European equities advanced between 2% and 3%, while Asian markets posted outsized gains, with Japan and South Korea rising as much as 5% and 8%, respectively. On Wall Street, the rally was reinforced by strong sentiment spillovers, including renewed enthusiasm around AI after SpaceX confidentially filed for what could become one of the largest IPOs in history, adding a further tailwind to risk appetite.

Across other asset classes, moves were more contained. Bond markets were largely unchanged, suggesting limited repricing of the macro outlook despite the equity surge. In FX, the $ edged slightly lower, with the DXY Index slipping back below the 100 level and remaining broadly flat over the past week.

Overall, markets are increasingly pricing a de-escalation scenario, though much hinges on upcoming political developments and confirmation that diplomatic signals translate into concrete actions.

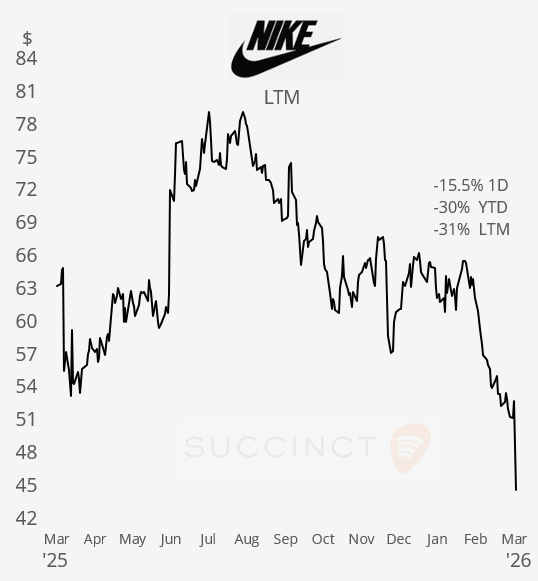

Notable mover: Nike (mcap $66bn) plunged 15.5% today to an 11-year low following yesterday evening’s earnings release. Despite an EPS beat, flat revenues and a weak outlook overshadowed results. China remains the key drag, with sales down 11% and expected to fall ~20% next quarter, while management flagged geopolitical risks and rising oil prices as headwinds. Guidance points to low-single-digit revenue declines and flat earnings, reinforcing that Nike’s turnaround remains slow and lacking near-term catalysts.

Business News: → Anthropic (unlisted), scrambled to contain an accidental leak of hundreds of thousands of lines of source code and internal instructions for its Claude AI agent, exposing product architecture and unreleased features to competitors despite no user data being compromised.

Economics: → US ISM Manufacturing PMI rose to 52.7 (in line with expectations), marking the strongest expansion since mid-2022 and a third consecutive month above 50. Activity remains in steady expansion, but the details were mixed, new orders softened, and employment stayed weak, while a sharp rise in input prices highlights building inflation pressures.

→ US retail sales rose +0.6% MoM and +3.8% YoY, indicating a solid rebound from prior softness. Consumer demand remains resilient on a yearly basis, though rising fuel costs pose a potential headwind.

Deals: → KKR plans to take Japan’s Taiyo Holdings (mcap $3.3bn) private in a ~$3.2bn deal via a tender offer, backed by major shareholders including DIC, Kowa and Oasis. Taiyo is a leading maker of solder resist (insulation materials for semiconductor circuit boards), positioning the deal as a bet on chip supply chain materials with support from the founding family reinvesting alongside KKR.

→ In private markets, Carlyle Group agreed to acquire a controlling stake in privately held MAI Capital Management, valuing the business at over $2.8bn. The deal builds on an existing relationship and aims to fund MAI’s expansion in integrated advisory services, reflecting strong structural demand for scaled wealth platforms serving high-net-worth clients.

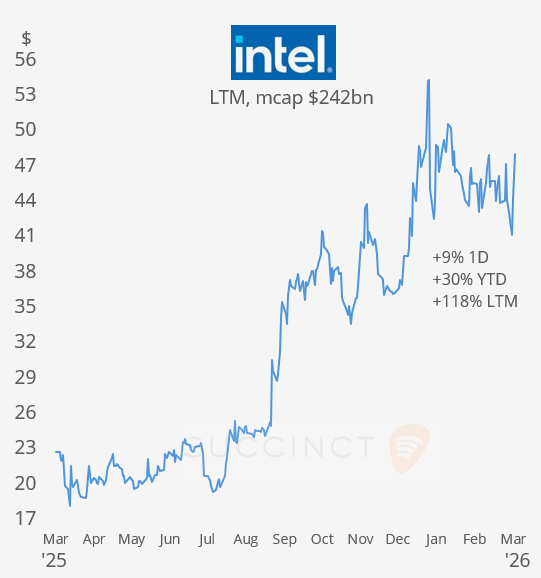

→ Intel (mcap $242bn) will acquire Apollo’s 49% stake in its Ireland Fab 34 facility for $14.2bn, fully consolidating the chip manufacturing asset. The deal, funded with cash and ~$6.5bn of new debt, unwinds Apollo’s 2024 financing and is expected to support Intel’s earnings and credit profile from 2027. Intel shares rallied 9% today and accumulated a 30% return YTD.

→ In IPOs, reusable rocket and space exploration company SpaceX confidentially filed for an IPO that could raise up to $75bn, implying a valuation well north of $200bn, with listing timing likely later this year pending SEC review.

Day Ahead:

Data → US initial (wkly) jobless claims, balance of trade; Switzerland inflation.

Earnings → n/a

See you tomorrow.

Copyright © 2026 Succinct.

All rights reserved. This publication contains proprietary content and is intended solely for the recipient’s personal use. Disclaimer: Our service is for informational purposes only and does not constitute personal financial advice.