Wed 11 Feb: After the Bell

Strong Jobs, Weak '25 Revisions: Markets Stay on Pause

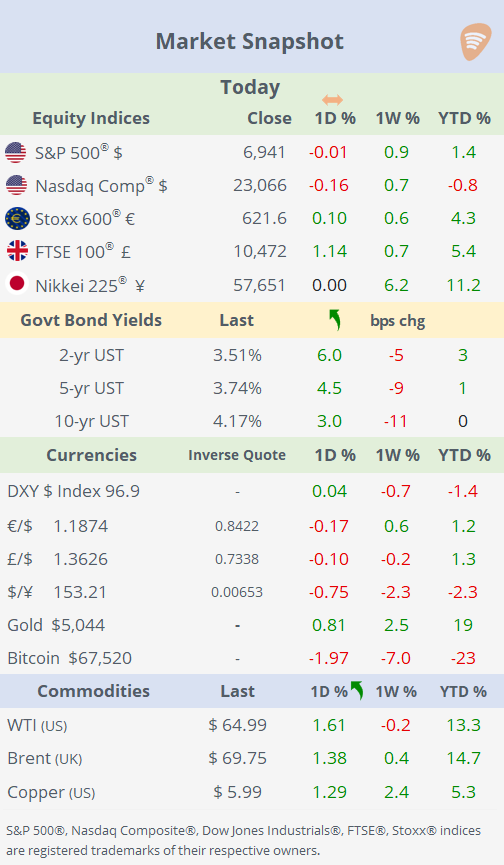

ℹ️Performance tables here.

Good evening,

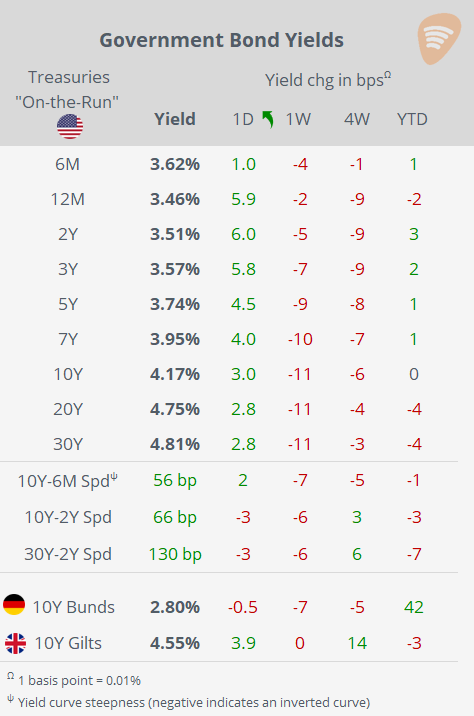

Markets traded largely sideways on Wednesday, with US equity indices and currencies showing little net movement, underscoring a cautious, wait-and-see tone. The main outliers were a rise in benchmark bond yields, a modest dip in crypto assets, and a small uptick in crude oil, while broader risk appetite remained subdued. This muted price action came despite a significant US labour market update, where headline January job gains surprised to the upside but were offset by heavy downward revisions to 2025 employment, leaving investors reluctant to reposition aggressively.

The US added 130,000 non-farm payrolls in January, well above the 70,000 expected, and the unemployment rate edged down to 4.3% from 4.4%, signalling near-term labour market resilience after a soft run of data. However, heavy downward revisions to 2025 payrolls cut annual job growth to 181,000 from 584,000, the weakest outside a recession since 2003, reinforcing the case for the Fed to keep rates on hold despite the headline beat.

Traders sharply pared back expectations for a 25bp Fed rate cut in mid-March, with the implied probability falling from 20% yesterday to 8% today, leaving markets pricing a 92% chance of no policy change.

Earnings: → Earnings were in focus, with several high-profile releases driving notable moves. Shopify shares fell 7% pre-market after results and guidance disappointed expectations, as investors focused on margin pressure and a more cautious outlook despite solid revenue growth. Cisco slid about 5% in extended trading after the close, weighed down by softer forward guidance and lingering concerns over enterprise and networking demand. Elsewhere, T-Mobile (+5%), TotalEnergies (+4%) and Heineken (+4%) traded higher on better-received results, while AppLovin slipped roughly 5% after hours.

Corporate Deals: → QXO (mcap $18bn), the US-based building products consolidator, agreed to acquire privately held Kodiak Building Partners, a Colorado-based distributor of lumber and construction materials, in a $2.25bn cash-and-stock deal. QXO shares jumped 17% today and are 38% higher YTD.

→ Activist hedge fund Elliott has taken a stake in London Stock Exchange Group (mcap £37bn), pushing for higher margins and increased share buybacks as the stock remains under pressure (-37% LTM) amid concerns that AI could disrupt demand for financial data and analytics, which accounted for 44% of LSEG’s Q3’25 revenue.

→ In IPOs, SOLV Energy, a San Diego, California–based infrastructure services provider focused on utility-scale solar and battery storage projects, priced its US IPO today at $25 per share, raising $512mn and securing a valuation of roughly $6bn as its shares debuted on the Nasdaq under the symbol MWH. Shares gained 23% on their debut.

→ São Paulo-based AGI Inc, a Brazilian fintech and consumer digital bank that provides technology-driven financial services and credit to underserved segments, priced its IPO at $12 per share, raising $240mn by selling 20mn shares. The offering valued the company at $1.9bn at pricing, significantly below earlier targeted ranges after the deal was downsized amid challenging market conditions. Shares lost 10% on their debut.

Day Ahead:

Data → US existing home sales and initial jobless claims; UK GDP; India CPI. Earnings → Applied Mat, Arista Net, Airbnb, Coinbase, Unilever, Siemens, Hermes, L’Oreal, Mercedes-Benz.

See you tomorrow.

Copyright © 2026 Succinct.

All rights reserved. This publication contains proprietary content and is intended solely for the recipient’s personal use. Disclaimer: Our service is for informational purposes only and does not constitute personal financial advice.