Wed 11 Mar: After the Bell

Energy Shock Drives Markets as Hormuz Traffic Disrupted | US CPI | Deals

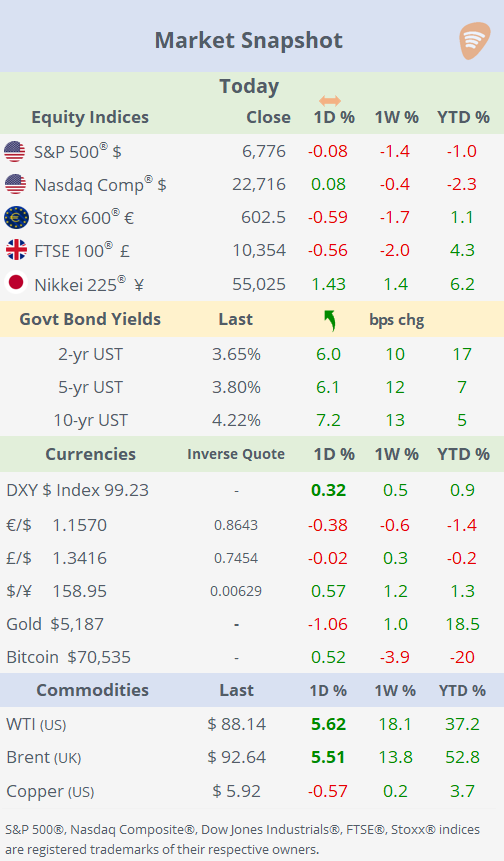

ℹ️Today’s performance tables.

Good evening,

Markets remain dominated by geopolitical developments as tensions around the Strait of Hormuz escalate, with tanker traffic still severely disrupted. Oil prices rebounded sharply, with Brent rising 5.5% to over $92 per barrel, leaving crude roughly 30% above pre-war levels despite a record 400mn-barrel reserve release by the International Energy Agency, equivalent to about four days of global demand (~104mn b/d).

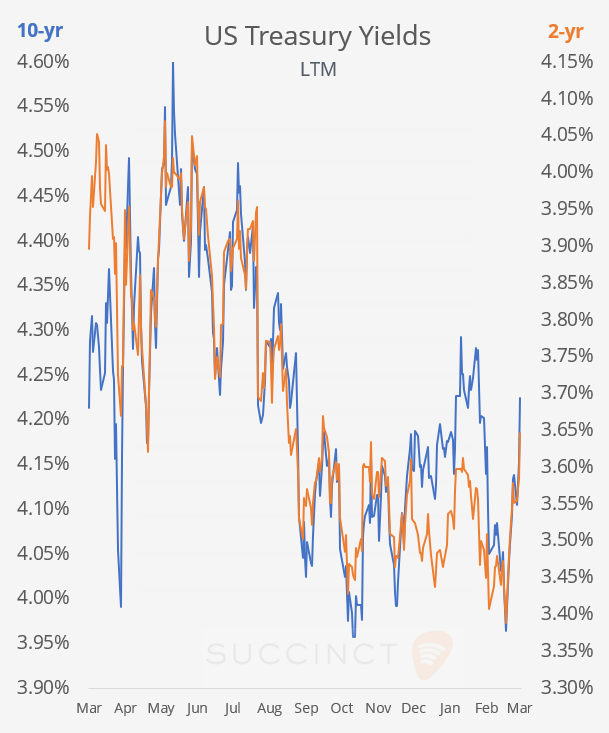

Meanwhile, reports of attacks on commercial vessels and US strikes on Iranian mine-laying boats underscored the fragility of shipping through the key energy corridor, which carries ~20% of global oil flows. Rising oil prices pushed bond yields higher on renewed inflation concerns, with traders now pricing just one rate cut this year from the Fed ahead of next week’s FOMC meeting, as the 2-year Treasury yield climbed to its highest level since late September.

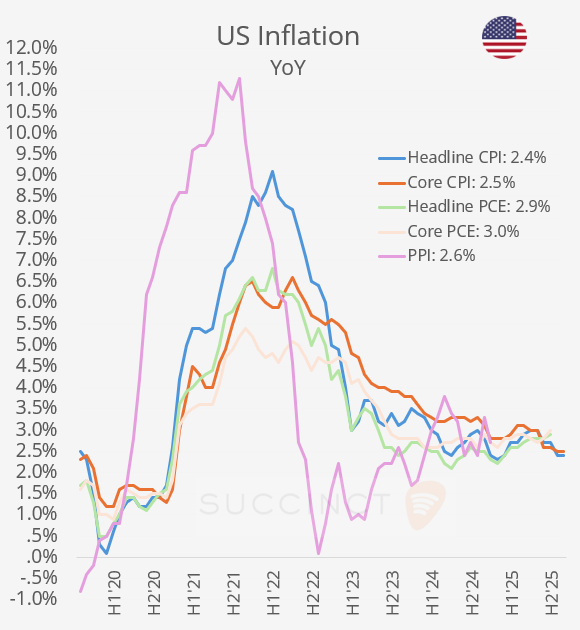

Economics: → US inflation was in line with expectations, with headline CPI rising 2.4% YoY in February (unch from January) and core CPI at 2.5%, also matching forecasts. Monthly core CPI came in at a tame 0.20%, reinforcing the recent disinflation trend and supporting the Fed’s current wait-and-see stance on rates.

However, the report is increasingly seen as a baseline rather than a forward signal, as the US–Iran conflict has pushed oil prices sharply higher, raising the risk of stronger inflation prints in the coming months. Meanwhile, policymakers remain focused on the PCE price index, which has been running at 2.9%, suggesting underlying inflation may still be somewhat hotter than CPI indicates.

→ US home sales show modest rebound: existing home sales increased 1.7% MoM in February to a 4.09mn annualised rate, though they remained 1.4% lower than a year ago. Tight inventory and elevated mortgage rates continue to weigh on housing demand, while the median home price rose 0.3% YoY to $398k.

Earnings: → Outside the US, earnings from Inditex (Zara, annual profit of €6.2bn), Porsche AG (confirmed a weak 2025) and Foxconn (continues to benefit from strong AI-server demand) were largely in line with expectations, with no major surprises reported or stock reactions.

Corporate Deals: → In the US industrials sector, Cintas Corp (mcap $80bn) agreed to acquire rival uniform supplier UniFirst (mcap $5bn) in a $5.5bn enterprise value deal, offering $310/share in cash and stock after multiple previous takeover attempts. Cintas expects the merger to generate $375m in operating cost synergies within four years by integrating route networks, supply chains, and service infrastructure. UniFirst shares rose 7% today and 44% YTD.

→ Kentucky-based pizza chain, Papa John’s International (mcap $1.25bn), is reviewing a $1.5bn take-private bid from Irth Capital, a Qatari-backed fund with support from Brookfield A.M. The offer of $47 per share, a ~50% premium to the pre-bid price, sent Papa John’s shares sharply higher after the news. Papa shares recovered 19% today, but are still 16% lower in the LTM.

→ In Italy’s banking sector, Banca Monte dei Paschi di Siena (mcap €23bn) reached an agreement on merger terms with Mediobanca (€13bn), offering 2.45 shares for each Mediobanca share in a deal expected to close by year-end and result in Mediobanca’s delisting. Monte Paschi, which already owns 86% of Mediobanca, plans to issue up to 272m new shares (~9% of capital) to complete the merger, diluting existing shareholders.

→ In IPOs, PayPay, the Japanese payments platform backed by SoftBank, is expected to price its US IPO near the low end of the $17–20 guidance range, implying a valuation of up to $13bn, despite demand reportedly over five times oversubscribed. Cornerstone investors, including Tencent, Ant Group’s Alipay, and Alphabet’s Google, have committed to the deal, with final pricing expected after market close today, suggesting trading could debut as early as tomorrow on Nasdaq (PAYP).

Day Ahead:

Data → US initial jobless claims, housing starts; India, Brazil inflation; Turkey policy rate.

Earnings → Adobe, BMW, RWE, Daimler, Generali.

See you tomorrow.

Copyright © 2026 Succinct.

All rights reserved. This publication contains proprietary content and is intended solely for the recipient’s personal use. Disclaimer: Our service is for informational purposes only and does not constitute personal financial advice.