Wed 15 Apr: After the Bell

Stocks Surge to Records on Calmer Middle East Backdrop

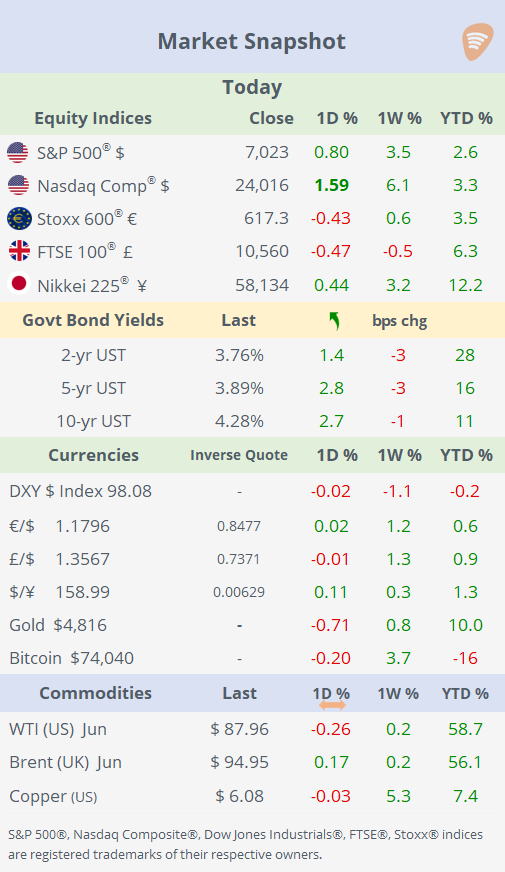

📈 Today’s performance tables.

Good evening,

Risk assets extended their relief rally on Wednesday as Middle East tensions appeared to pause, with no major new escalation from Iran or fresh Hormuz disruption headlines. The focus shifted toward diplomacy and shipping logistics, allowing investors to take comfort from a quieter geopolitical backdrop after several sessions of conflict-driven volatility.

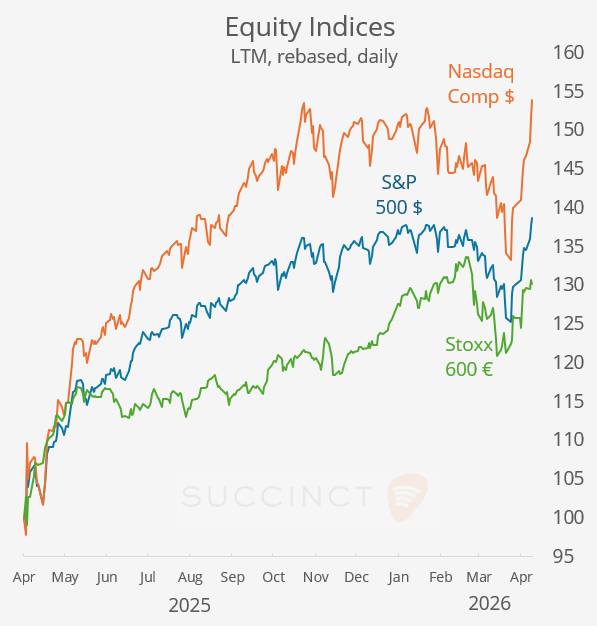

US equities responded strongly, with the S&P 500 and Nasdaq hitting a new record high, fully recovering losses linked to the Iran shock. Leadership again came from mega-cap growth, as the Magnificent-7 rose 2.6%, bringing its gain to 9% over the past week. Individual standouts included Microsoft (+4%) and Tesla (+7%), reflecting renewed momentum in tech names.

Investors are now looking for signs of progress in US–Iran talks, which could further extend the rebound in risk assets. Analysts are also digesting another busy stretch of Q1 earnings season, with major financial institutions continuing to report results.

Central Banks: → Trump renewed threats to fire Jerome Powell if he remains after his term ends on May 15, while also saying a Justice Department probe into the Fed chair over headquarters renovations will continue. The comments add fresh uncertainty around Federal Reserve independence and leadership succession, with Powell indicating he would stay until a successor is confirmed if needed.

Economics: → Wednesday was a light day on the data front. €-zone industrial production rose 0.4% MoM in February, rebounding from -0.8% in January, while the annual rate was -0.6% YoY, better than expectations for a steeper decline and signalling some stabilisation in the manufacturing sector. The tone is modestly positive but still fragile.

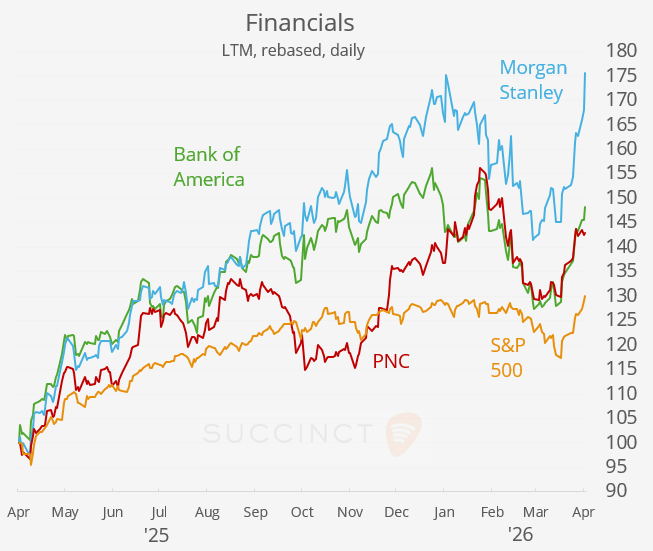

Earnings: → Today’s bank earnings were constructive overall, with all three names beating estimates and shares trading higher, led by Morgan Stanley.

Bank of America beat forecasts as Q1 profit rose to $8.6bn, helped by strong trading and investment-banking fees; equities trading hit a record, and shares moved higher.

Morgan Stanley delivered the standout report, with record revenue of $20.6bn, driven by record equities trading and record wealth-management revenue; the stock outperformed peers.

PNC also beat expectations, supporting the broader positive tone for financials.

Earnings season for banks remains solid, with trading strength and dealmaking offsetting macro concerns.

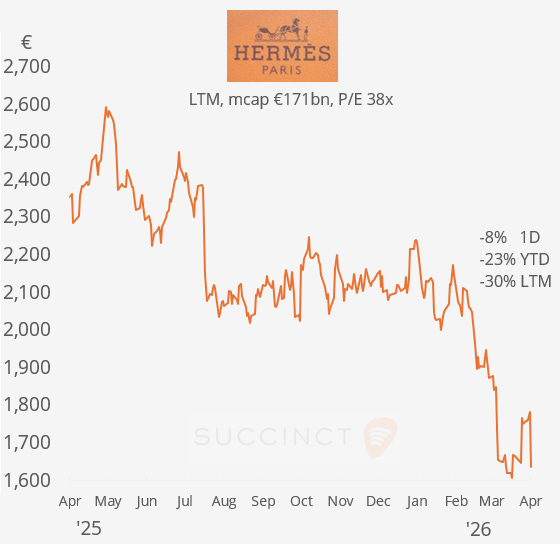

→ Shares of French luxury goods maker Hermès (mcap €171bn) slumped 8% to the lowest level since Oct ‘23 after Q1 sales disappointed, with revenue at €4bn and constant-currency growth of 5.6%, below the 7.1% expected, as the Iran war disrupted luxury demand. The company cited weaker tourist flows and a significant hit to Gulf-region sales, reinforcing a broader sector slowdown already seen at Kering and LVMH.

Business News: → Alphabet is reportedly sitting on a potential $100bn+ windfall from its early investment in SpaceX, after new filings showed Google held a 6.11% stake at end-2025; at a $2tn valuation, that stake could be worth roughly $122bn.

Deals: → Aegon (mcap $12bn), owner of insurer Transamerica, is selling its UK insurance unit to Standard Life for $2.7bn (£2bn) to pivot toward US life insurance and retirement dominance. The deal yields Aegon a 15.3% stake in Standard Life plus £750mn cash. Standard Life emerges as the UK’s top retirement savings provider for 16mn customers.

→ Private equity firm American Industrial Partners (AIP) agreed to acquire Georgia-based medical devices specialist Avanos Medical (mcap $1.1bn) in a $1.3bn take-private deal, focusing on scaling its chronic pain and clinical nutrition platforms. Shares rallied 60% premarket on the announcement but ended flat on the day. Shares are 77% higher in the past week.

Day Ahead:

Data → China’s macro data out overnight; UK GDP, industrial production; US industrial production and initial jobless claims.

Earnings → Netflix (PM), Pepsico, Abbott, Schwab, BNY Mellon, US Bancorp, Prologis.

See you tomorrow.

Copyright © 2026 Succinct.

All rights reserved. This publication contains proprietary content and is intended solely for the recipient’s personal use. Disclaimer: Our service is for informational purposes only and does not constitute personal financial advice.