Wed 17 Dec: After the Bell

AI Funding Fears Spark Risk-Off Sell-Off on Wall Street.

ℹ️ Today’s performance tables & charts on the ‘Market Data’ post.

ℹ️ USMD will take a break until early January. A big thanks to our subscribers🙏 Merry Christmas🎅

Good evening,

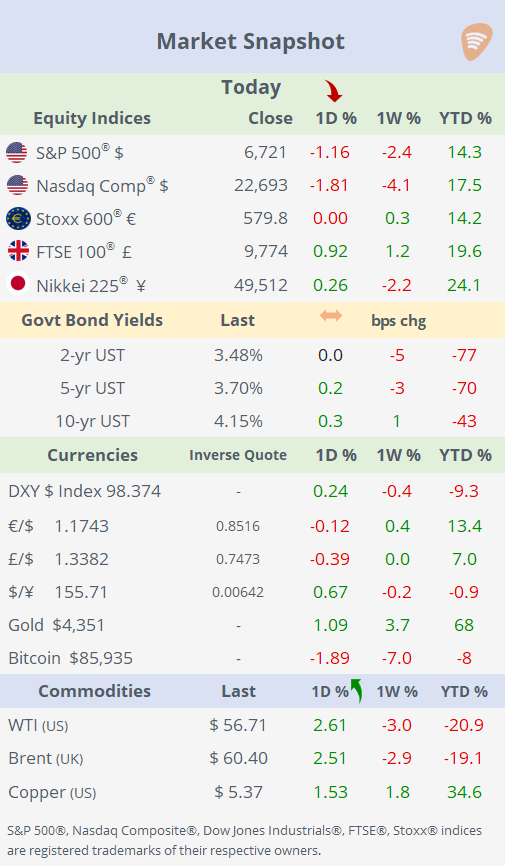

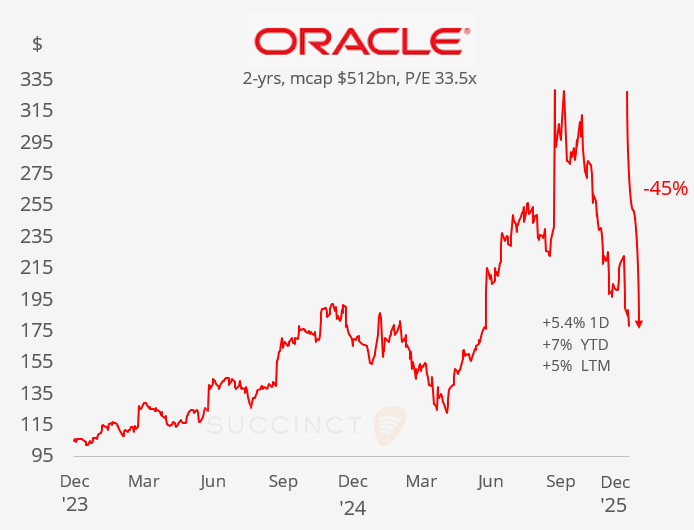

It was a clear risk-off session on Wall Street, with the Dow, S&P 500 and Nasdaq falling between 1% and 2% as renewed pressure on technology stocks weighed on sentiment. The sell-off was triggered by fresh concerns around the AI trade after a Financial Times report said Oracle’s $10bn data-center project had lost backing from US private lender Blue Owl Capital, reviving scrutiny of rising leverage and off-balance-sheet financing used to fund AI infrastructure amid lingering questions over end demand.

Oracle shares slid nearly 6%, dragging megacap tech lower, with Nvidia down almost 4%, Broadcom off more than 4% and Google falling over 3%, while the MAGS index dropped 2.2%. Energy was the standout sector, supported by a partial rebound in crude oil prices after a weak week. Investors also remained cautious ahead of Thursday’s US consumer inflation data, while continuing to digest yesterday’s delayed and mixed non-farm payrolls release.

In commodities, geopolitical headlines lifted oil prices, as Trump ordered a “total and complete” blockade of sanctioned Venezuelan oil tankers, easing oversupply concerns even as Russia-Ukraine peace talks raised the prospect of increased Russian output.

Earnings: → Micron Technology (mcap $254bn) reported quarterly results after the close that beat both top- and bottom-line estimates, with revenue up 57% YoY and profit soaring 167% YoY and provided a strong outlook for the next quarter. Despite shares closing 3% lower in regular session trading, the stock recovered strongly in extended hours, rising more than 7% as investors reacted to the better-than-expected performance and guidance.

Data: → The UK’s headline CPI inflation slowed to 3.2% YoY in November, down from 3.6% in October, marking the lowest annual rate in several months and well below market forecasts. On a monthly basis, CPI fell by about 0.2%, reversing the prior month’s increase and suggesting broad disinflationary pressures. Core CPI inflation also eased to 3.2% YoY from 3.4%, reinforcing the trend of moderating underlying price pressures as the Bank of England weighs further rate cuts.

Deals: → UWM Holdings (mcap $8bn) agreed to acquire REIT Two Harbors Investment in a $1.3bn all-stock transaction, offering a roughly 21% premium as US mortgage lenders continue to consolidate to strengthen scale and earnings. UWM shares fell 6% while Two Harbors jumped 12%, though its shares remain down about 6% year to date.

→ In IPOs, Medline Inc., a major US medical supplies manufacturer and distributor, priced its IPO at $29 per share within a marketed range of roughly $26–30, selling 216mn shares and raising $6.3bn in the largest initial public offering of 2025. Shares jumped 41% on their debut to a $70bn total market value. Backed by Blackstone, Carlyle and Hellman & Friedman, the deal’s strong pricing and robust investor demand underscore renewed IPO market momentum, especially for private equity-sponsored listings.

→ Also, Andersen Group, the US tax, valuation and financial advisory firm founded by former Arthur Andersen partners, priced its IPO at $16, the top of a $14–16 guidance range, raising $176mn at a $1.8bn valuation. Shares rallied 45% on their debut. These IPOs caps the 2025 calendar and reflect renewed investor appetite for professional services listings.

Day Ahead: → Monetary Policy meetings: Bank of England (-25bp to 3.75% exp); ECB (unch at 2.15% exp); Mexico (-25bp to 7% exp).

→ Data: US & Japan CPI inflation.

→ Earnings: Nike, Cintas, FedEx.

Copyright © 2025 Succinct.

All rights reserved. This publication contains proprietary content and is intended solely for the recipient’s personal use. Disclaimer: Our service is for informational purposes only and does not constitute personal financial advice.