Wed 18 Feb: After the Bell

Fed Minutes Expose Rate Divide as Stocks Push Higher. What you need to know in 4 mins:

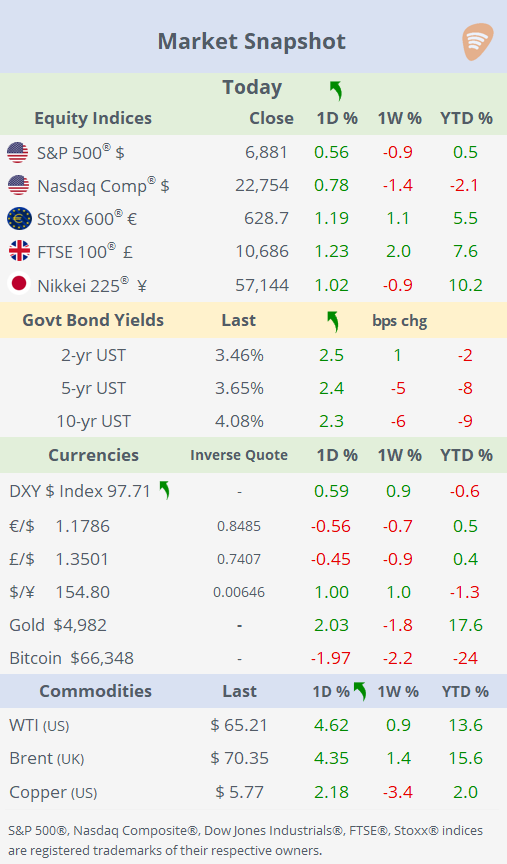

ℹ️ Today’s tables & charts on the ‘Market Data’ post.

Good evening,

The Fed’s FOMC minutes were the key macro focus, revealing a clear internal divide on the rate path. Some officials see scope for further cuts if inflation cools, while others favour holding rates “for some time,” warning that progress toward the 2% target could be slower and uneven, with a meaningful risk of inflation staying persistently above target. Markets responded by dialling back near-term easing expectations, bonds fell, the $ rallied broadly (with the ¥ the weakest), though futures still imply a first cut by June.

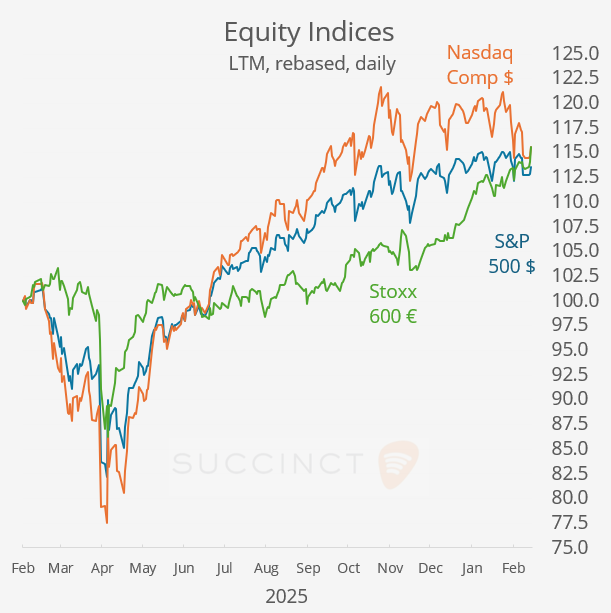

Against this backdrop, US equities finished higher, led by a rebound in AI-linked tech and growth stocks that lifted the S&P 500 and Nasdaq, supported by stabilising macro data and confidence in a patient Fed. European equities hit fresh all-time highs, with the STOXX 600 leading gains as cooling inflation reinforced rate-cut expectations, boosting banks and cyclicals while easing valuation pressures.

In commodities, crude oil rallied >4% today as geopolitical risk repriced the market, with stalled US–Iran nuclear talks and the failure of peace talks between Ukraine and Russia reigniting concerns about potential supply disruptions and keeping a risk premium on crude.

Earnings: → Releases today: Analog Devices posted strong Q1 results and an outlook, topping revenue and EPS estimates and raising its dividend amid robust industrial and data-centre demand, lifting its stock ahead of the open. Moody’s beat Q4 sales and earnings expectations with solid growth and upbeat 2026 guidance, while Glencore reported a modest earnings dip but announced a $2bn shareholder return, supporting gains in both names.

→ Large software companies that reported yesterday after the close: Palo Alto Networks (mcap $122bn) beat Q2 revenue and earnings estimates. Still, they saw its stock slide after cutting full-year profit guidance and issuing a softer near-term EPS outlook, as acquisition costs weigh on margins and investor focus shifted to guidance.

In contrast, Cadence Design Systems (mcap $83bn) reported stronger-than-expected revenue and profit, driven by robust AI-linked demand and a raised outlook, lifting its shares by over 7%.

Economics: → FOMC Minutes from January’s meeting: The Fed struck a cautious, mildly hawkish tone, acknowledging stabilising labour conditions and solid growth while warning that disinflation could be slower and uneven, with some officials even keeping rate hikes on the table in extreme scenarios. Notably less dovish than markets hoped, but with two-sided guidance emerging, cuts remain possible if inflation falls, though most policymakers stressed upside inflation risks remain meaningful.

Today’s US macro releases, durable goods orders, housing starts, building permits and industrial production, painted a mixed-to-soft picture, with manufacturing and housing activity remaining below trend and lacking momentum. There were no surprises, reinforcing a gradual cooling narrative and aligning with the Fed’s patient, data-dependent stance.

Traders priced in a 94% probability that policy rates will remain unchanged, reflecting growing confidence in a steady stance at the Fed’s meeting in March.

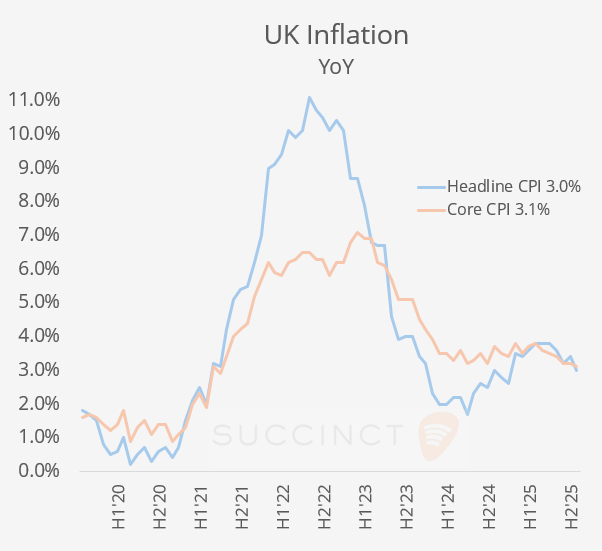

→ The UK’s January inflation report showed headline CPI easing to 3.0% YoY (from 3.4% in December) and core CPI moderating to 3.1% YoY, while prices fell 0.5% MoM, reflecting broad disinflation across transport, food and services. The print was softer than earlier readings and in line with expectations, reinforcing market bets on an imminent Bank of England rate cut, though underlying services inflation remains sticky above target.

Corporate Deals: → In private markets, Blackstone is to acquire Champions Group, a provider of essential home services, from Odyssey Investment Partners, in a deal reportedly valuing the Orange County, California-based business at around $2.5bn.

→ In the UK telco sector, owners of Virgin Media O2 (Liberty Global, Telefónica and PE firm InfraVia) agreed to acquire privately held Substantial Group for ~£2bn from Advencap, DigitalBridge and Soho Square Capital, bolstering UK fibre infrastructure to challenge BT Openreach.

Day Ahead:

Data → US pending home sales, initial jobless claims, balance of trade; Japan inflation; China loan prime rates; Indonesia central bank rates. Earnings → Walmart, Alibaba, Airbus, Deere, Southern, Constellation Energy.

See you tomorrow.

Copyright © 2026 Succinct.

All rights reserved. This publication contains proprietary content and is intended solely for the recipient’s personal use. Disclaimer: Our service is for informational purposes only and does not constitute personal financial advice.