Wed 18 Mar: After the Bell

Inflation Fears Resurface as Oil Jumps and Yields Spike; Fed meeting 🎯

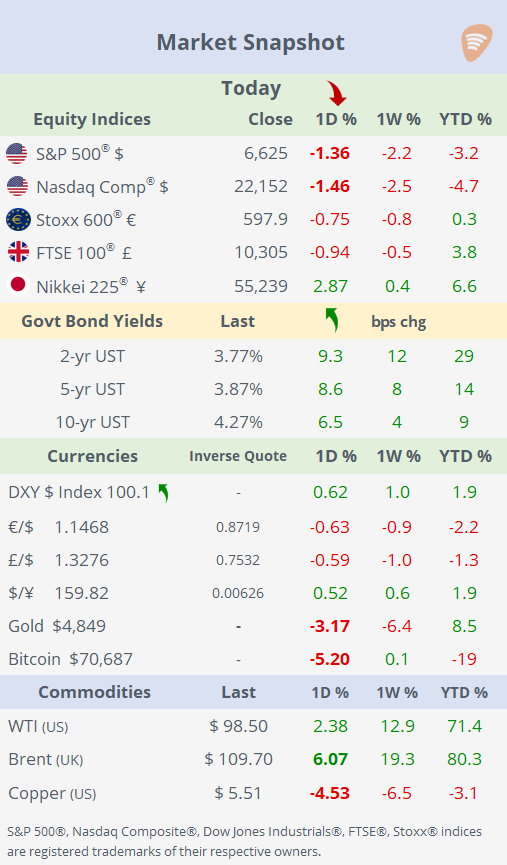

ℹ️ Today’s performance tables.

Good evening,

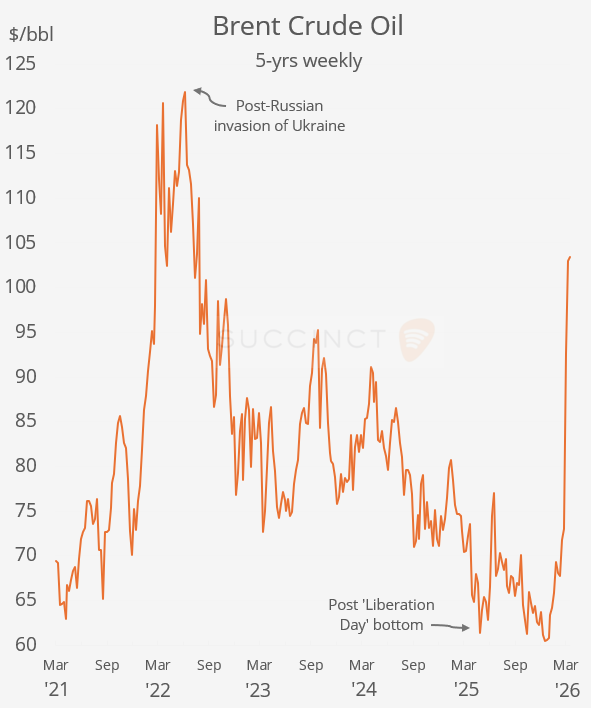

Global markets saw a notable shift to risk-off as geopolitics and monetary policy collided. Tensions escalated after Israel struck Iran’s South Pars gas field, the world’s largest, while Tehran retaliated by targeting regional energy infrastructure, raising concerns over supply disruptions across the Gulf. Oil surged, with Brent jumping 6% to around $110, its highest since mid-2022, intensifying fears of a renewed energy shock feeding into global inflation.

Against this backdrop, the Federal Reserve reinforced a more cautious tone. Jerome Powell warned that rising energy prices could lift inflation expectations and weigh on growth, adding to pressure from hotter wholesale inflation data (PPI). The combination of geopolitical uncertainty and inflation risks is challenging the credibility of the Fed’s easing path, with markets increasingly questioning whether rate cuts can materialise as previously signalled.

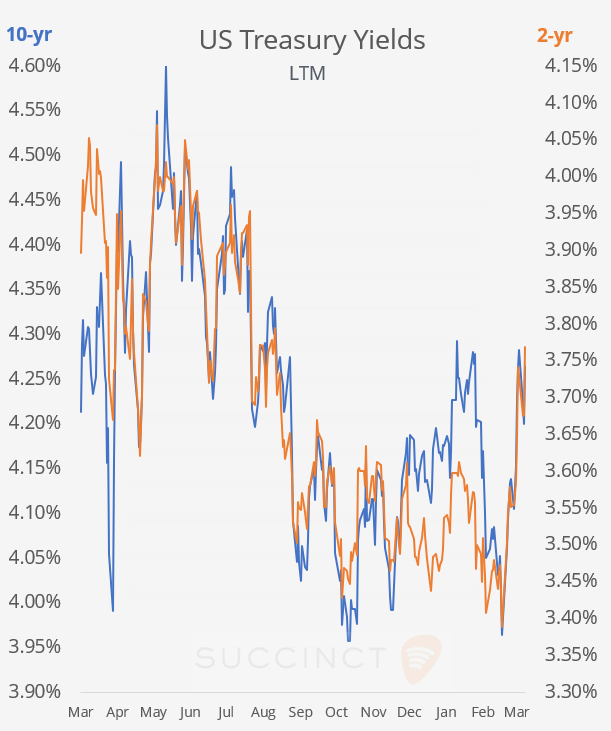

Asset prices reflected this shift decisively: equities sold off into the close, Treasury yields jumped sharply (2-year at ~3.77%, highest since August), and the $ index moved back above 100. Higher yields and tighter financial conditions weighed broadly, with Bitcoin falling over 5% and gold retreating, while copper dropped more than 4% to multi-month lows amid weaker Chinese demand, rising inventories, and macro headwinds.

After the close, Micron Technology (mcap $520bn) delivered strong Q2 results and upbeat guidance, beating expectations on both revenue and earnings as AI-driven demand for memory chips remains robust. Despite the strong fundamentals and a powerful rally over the past year, the stock slipped 2% in extended trading.

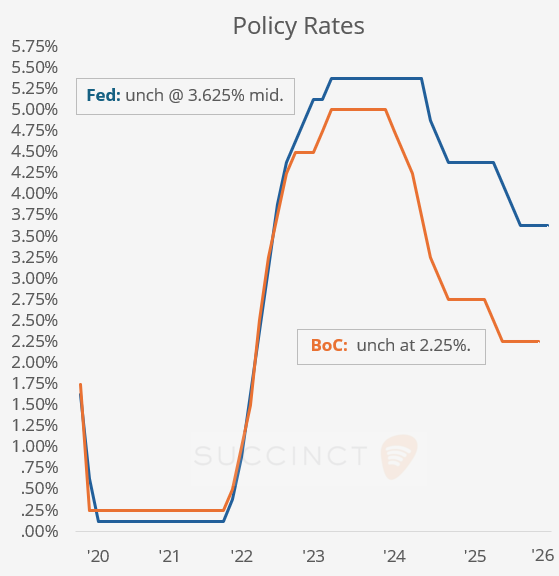

Monetary Policy: → The Fed held rates steady (11–1 vote) at a 3.5-3.75% range as widely anticipated, and kept the median dot plot unchanged, still signalling one rate cut this year, in line with prior guidance. Updated projections showed higher inflation (PCE 2.7% vs. 2.5%) alongside solid growth (+2.4% GDP), while some participants shifted toward fewer cuts and a few even signalled upside risks to rates.

Policymakers flagged increased uncertainty stemming from the Iran conflict, noting that rising oil prices are lifting near-term inflation expectations, though Powell stressed it is too early to assess the duration or magnitude of the shock. Despite this, the Fed maintained its baseline easing bias, signalling it still expects to cut rates once conditions allow. The meeting was Powell’s penultimate as chair, though he said he could stay on longer than planned if his successor hasn’t yet been confirmed.

Bottom line: not a clear hawkish pivot, but a “cautious hold” as the Fed is still leaning toward cuts, yet rising energy-driven inflation risks are pushing easing further out and raising uncertainty around the path.

→ The Bank of Canada held rates unchanged at 2.25%, in line with expectations, maintaining a cautious pause amid a still-soft growth backdrop. Policymakers signalled a balanced but slightly hawkish stance, noting that while inflation is near target, rising oil prices pose upside risks, leaving the door open to hikes if price pressures prove persistent.

Economics: → US producer prices came in hotter than expected, with headline PPI rising 3.4% YoY (up from 2.9% previously) and core PPI at 3.9% YoY, both above consensus. The data point to re-accelerating pipeline inflation, driven in part by energy and services, suggesting price pressures are not easing as expected and complicating the disinflation trend.

→ US factory orders rose just 0.1% MoM and were up ~3.5% YoY, pointing to modest, uneven manufacturing momentum rather than a strong rebound.

Corporate Deals: → It was a quiet day on the M&A front, with no significant deals announced.

→ Kraken has paused its multibillion-dollar IPO plans, opting to delay a potential listing amid uncertain market conditions despite ongoing internal preparations. The crypto exchange is still considering going public, but is likely to wait for stronger equity and digital asset market sentiment before proceeding.

Day Ahead: Another busy session for central banks.

Monetary Policy → ECB, Bank of England, Bank of Japan, Swiss National Bank and China’s LPRs. (all expected to remain steady).

Data → US new home sales; UK employment.

Earnings → FedEx, Enel, Alibaba.

See you tomorrow.

Copyright © 2026 Succinct.

All rights reserved. This publication contains proprietary content and is intended solely for the recipient’s personal use. Disclaimer: Our service is for informational purposes only and does not constitute personal financial advice.