Wed 25 Mar: After the Bell

Markets Caught Between Escalation Risks and Truce Hopes

Good evening,

Markets remain highly reactive this Wednesday, with sentiment still dominated by the evolving conflict in the Middle East. After several sessions of sharp swings, risk assets found some footing as crude, particularly Brent, pulled back on tentative hopes of a de-escalation, even as the situation on the ground remains fluid. Headlines point to a fragile mix of diplomacy and escalation risk, with the White House warning of further strikes absent a deal, while Iran continues to reject overtures despite ongoing talks. The result is a market still trading headline-to-headline, with volatility elevated across asset classes.

At the core of the current macro dynamic is oil, and its direct transmission into inflation and rate expectations. The recent spike and subsequent pullback in energy prices have been the key drivers behind shifting views on the policy path of the Federal Reserve and other central banks. Traders are effectively toggling between two scenarios: further escalation pushing oil higher and delaying rate cuts, versus a credible ceasefire easing inflation pressures and allowing for policy normalisation. Until there is greater clarity on the geopolitical front, markets are likely to remain unstable, with oil acting as the primary conduit into broader macro pricing.

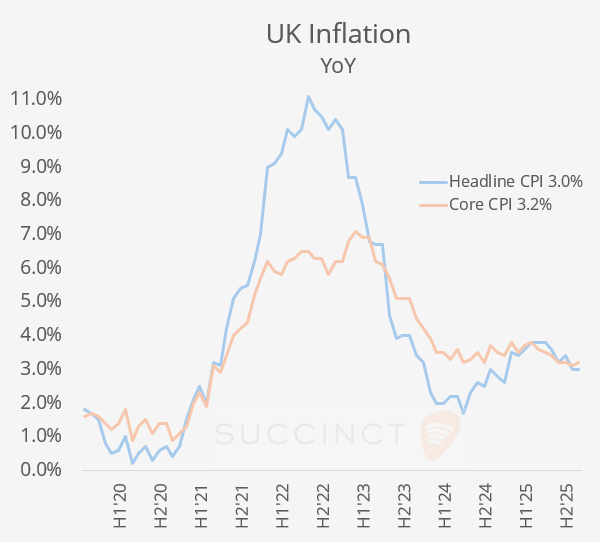

Economics: → UK headline CPI inflation rose +0.4% MoM and +3.0% YoY, broadly stable and in line with expectations. Core CPI printed at 3.2% YoY (vs 3.1% prior and expected), indicating a slight upside surprise and suggesting underlying inflation pressures are not easing further. Overall, the data points to sticky core inflation, likely reinforcing a cautious stance from the Bank of England on the timing of rate cuts.

→ The US reported a Q4’25 current account deficit of -$191bn, narrower than expected and a marked improvement from -$239bn in Q3. The sharp contraction suggests a meaningful reduction in external imbalances, likely reflecting stronger net exports and/or income flows into year-end.

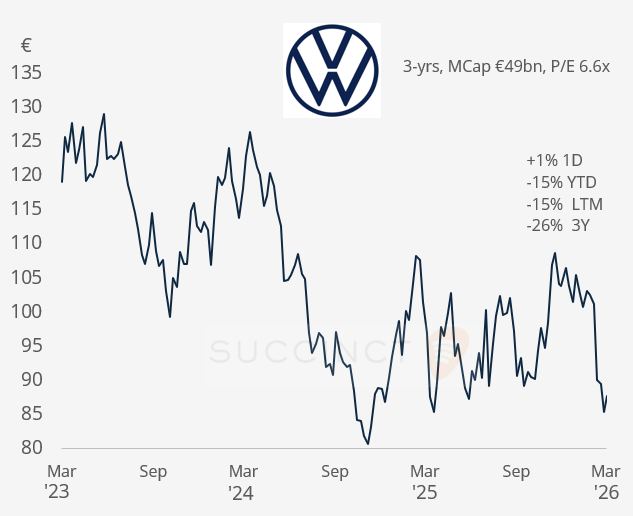

Business news: → Volkswagen (mcap €45bn) is in talks with Israel’s state-owned Rafael Advanced Defense Systems to repurpose a German plant for Iron Dome components, highlighting a potential shift from autos to defence manufacturing amid weak car demand.

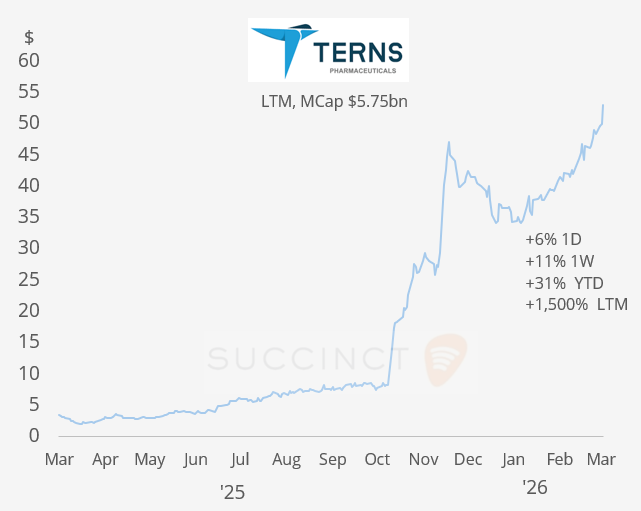

Corporate Deals: → In the US pharma sector, Merck & Co. (mcap $294bn) has agreed to acquire Terns Pharmaceuticals (mcap $5.7bn) for ~$5.7bn (or $53/share), gaining a promising experimental leukaemia treatment to strengthen its oncology pipeline. The deal reflects Merck’s push to offset the upcoming patent expiry of Keytruda in 2028, securing future growth through new cancer therapies. Terns shares gained 6% today and are +31% YTD.

→ In private markets, KKR and Global Infrastructure Partners (owned by BlackRock) are among bidders for French telecom infrastructure company XpFibre, with offers valuing the business at €6–8bn as Patrick Drahi explores asset sales. The process is part of efforts to reduce debt across Altice (>€50bn), highlighting continued investor appetite for core infrastructure assets despite tighter financing conditions.

→ Also, KKR has agreed to acquire retail bakery chain Nothing Bundt Cakes from Roark Capital for over $2bn (incl. debt), continuing PE interest in franchised, cash-flow stable consumer brands. The deal underscores the appeal of asset-light franchise models, with Nothing Bundt Cakes, founded in 1997 and now scaled to hundreds of locations, offering predictable revenues and expansion potential.

→ In IPOs, SpaceX is reportedly targeting up to $75bn in its IPO, which would make it the largest public offering ever and imply a valuation potentially exceeding $1.7tn. The deal underscores massive investor demand for space and satellite infrastructure (driven by Starlink) but would also mark a major shift toward greater transparency and public market scrutiny for one of the world’s most valuable private companies. SEC filing could happen as soon as this week or next, and listing is targeted around June 2026.

Day Ahead:

Data → US weekly jobless claims.

Monetary Policy → Mexico (unch at 7% exp), South Africa (unch at 6.75% exp).

Earnings → CNOOC, Bank of China.

See you tomorrow.

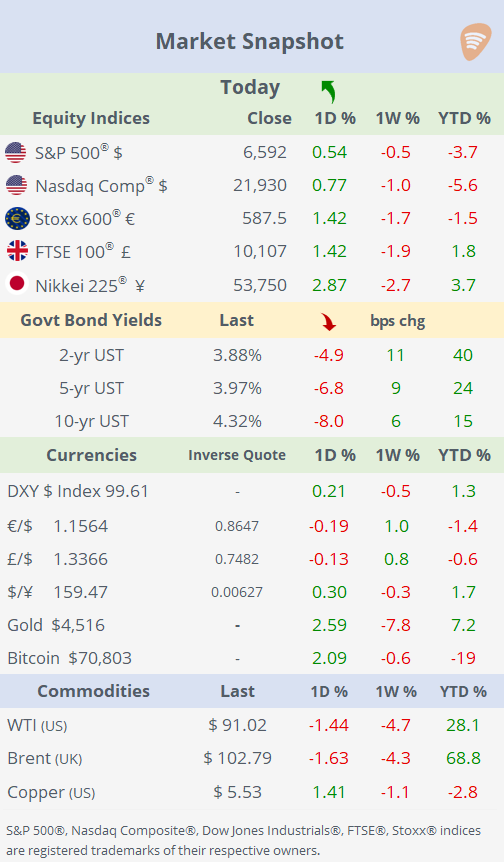

📈Today’s performance tables.

Copyright © 2026 Succinct.

All rights reserved. This publication contains proprietary content and is intended solely for the recipient’s personal use. Disclaimer: Our service is for informational purposes only and does not constitute personal financial advice.