Wed 28 Jan: After the Bell

Calm Fed Day, Flat Equities, Gold Up & a Late Earnings Jolt. Your 5’ evening market wrap➡️

ℹ️ Today’s tables & charts on the ‘Market Data’ post.

If you find USMD useful, we’d greatly appreciate it if you shared this post with colleagues or friends who may also find it valuable.

Good evening,

Markets digested a largely uneventful Fed day, with the central bank holding rates steady at its first meeting of 2026 in a split decision and Powell offering little guidance on the path ahead; core bond yields finished little changed. The $ partially stabilized after sliding to its weakest level since early 2022, as Trump brushed off concerns over currency weakness, while gold (+5%) and silver (+10%) accelerated their rally on renewed debasement fears, even as cryptocurrencies were broadly flat.

Equities traded sideways, with big tech outperforming small caps and the S&P 500 ending flat ahead of mega-cap earnings, while in extended trading Microsoft fell 5% despite beats, Meta jumped 5%, IBM 6% and Tesla 3% as results crossed after the close.

In geopolitics, Trump warned Iran that “time is running out” to reach a deal to avert US military action, signalling readiness to escalate pressure if talks fail. Secretary of State Rubio added that the Iranian regime is “probably weaker than it has ever been,” citing mounting economic and internal strains.

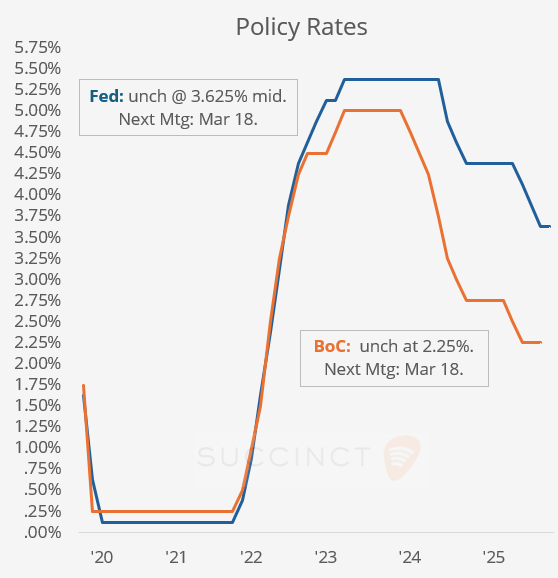

Monetary Policy: → The Fed held rates steady at 3.5%–3.75%, taking a cautious, slightly hawkish pause as it signaled little urgency to resume cuts after three reductions in late 2025, reflecting persistent inflation aboveits 2% target and solid economic expansion while markets had widely priced in no change.

Jerome Powell emphasized that the central bank remains data-dependent, balancing stable growth and labour market trends against inflation risks, without committing to the timing of future moves. The vote was 10–2, with governors Stephen Miran and Christopher Waller dissenting in favor of an immediate quarter-point cut, underscoring ongoing internal debate even as the majority adopts a neutral, wait-and-see stance. The Fed meets next on March 18, with traders pricing a 13% chance of a quarter-point cut and 87% of no change.

→ The Bank of Canada held its policy rate at 2.25% today, as widely expected, and signaled that elevated uncertainty, particularly from US trade policy, makes the timing and direction of its next rate move unclear, keeping options open while affirming the current rate remains appropriate for the outlook. The CAD barely moved today and is 1% stronger YTD.

Earnings: → This morning’s earnings saw AT&T jump 5% after reporting better-than-expected Q4 results, driven by strong wireless and fiber subscriber growth, solid revenue and a sizeable new $10bn buyback plan, boosting investor confidence. Starbucks was largely flat, with results showing healthy sales growth but mixed earnings outcomes, leaving the stock without a clear catalyst.

Economics: → Calendar was quiet today, with no major data releases to materially influence markets.

Business News: → US corporate cost-cutting remained in focus, led by Amazon’s plan to cut ~16,000 corporate roles, part of a broader efficiency and AI-driven restructuring that brings total announced reductions since late 2025 to roughly 30k jobs. The move highlights a wider trend of large US corporates continuing workforce reductions to streamline operations and protect margins amid slowing growth and shifting strategic priorities.

Corporate Deals: → Investment firm Stonepeak and French shipping group CMA CGM (privately owned) agreed to form United Ports, a $10bn US-based port venture covering 10 terminals globally, aimed at accelerating terminal investment and reducing China’s influence in global shipping. Stonepeak will invest $2.4bn for a 25% stake, with CMA CGM holding 75%, and may commit up to $3.6bn more for future port projects, with a strategic focus on the US.

→ Permira has formally launched the sale of German CNS-focused drugmaker Neuraxpharm, targeting a €3-4bn valuation, with non-binding bids due on Feb 5. Lenders are lining up up to €1.5bn in leveraged financing (around 5.5x–8x EBITDA) as banks and private credit firms compete to back the deal, supported by EBITDA expected to reach ~€230m this year.

Day Ahead:

Data: US jobless claims, balance of trade, factory orders. Earnings: Apple, Visa, Mastercard, Caterpillar, Thermo F, Blackstone, Comcast, SAP, Samsung.

See you tomorrow.

Copyright © 2025 Succinct.

All rights reserved. This publication contains proprietary content and is intended solely for the recipient’s personal use. Disclaimer: Our service is for informational purposes only and does not constitute personal financial advice.