Wed 4 Feb: After the Bell

AI Jitters Deepen as Tech Slides and Earnings Disappoint ...

ℹ️Find more performance tables here. (These are not emailed).

Good evening,

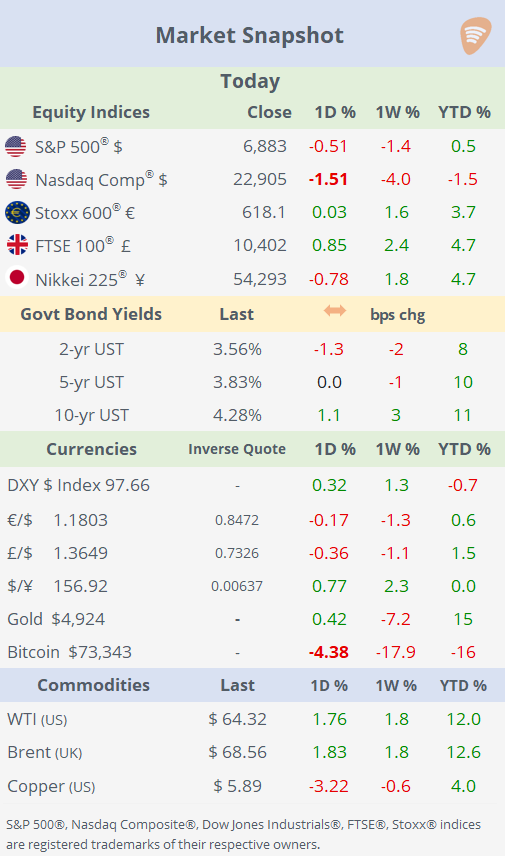

Investor sentiment remains firmly anchored to AI and software, but cracks are widening. The Nasdaq extended its decline, down 1.5% on the day and roughly 4% over the past week, as AI jitters rattled global tech stocks. Chipmakers came under renewed pressure, the IT sector sharply underperformed, and the MAGS ETF slid 3.7% over five sessions, while energy emerged as Wednesday’s best-performing sector and the Dow proved relatively resilient.

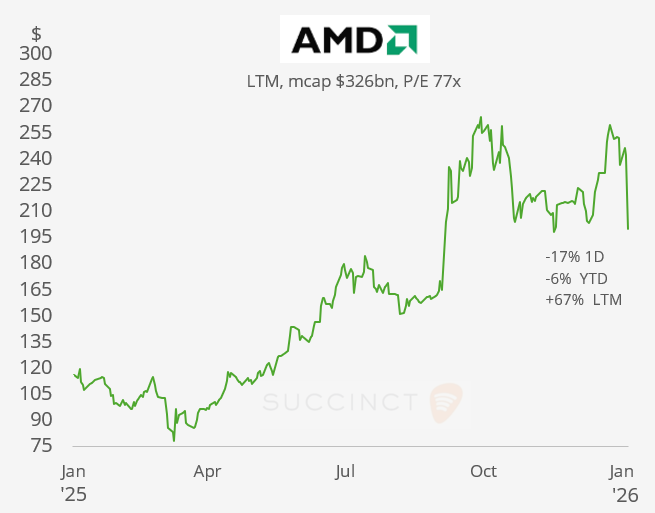

Earnings amplified the volatility: chip giant AMD plunged 17%, its worst session since 2017, despite beating Q4 revenues, as a cautious Q1 outlook disappointed investors amid lofty AI expectations. After the close, Alphabet beat estimates with shares edging 3% higher in extended trading, while Qualcomm sank 9%.

Across macro assets, the $ firmed mainly versus the ¥, crypto losses deepened with Bitcoin down 18% in seven sessions to $73,300, and core bond yields were little changed with the 10-year Treasury steady at 4.28%. In commodities, energy prices moved higher, copper fell 3%, and silver jumped 4.5%.

Earnings: → Mixed to poor today: Eli Lilly rallied 10% on blowout Q4 results and upbeat 2026 guidance fueled by Mounjaro/Zepbound demand outpacing rivals.

Novo Nordisk plunged 17%, confirming a grim 2026 sales outlook (-5-13% drop from US pricing pressures, Lilly competition, semaglutide generics), wiping out recent gains.

AbbVie (-3.5%), Uber (-5%), and Santander (-3.5%) also disappointed expectations; overall sentiment was negative for growth stocks amid pricing headwinds and softening demand signals.

Economics: → The US ADP Employment weekly change showed that private sector jobs rose by 22k, well below the ~46k forecast and down from the prior month’s 37k, a mild deceleration in job creation. The US ISM Services PMI for January held steady at 53.8, indicating continued expansion in the services sector.

→ €-zone’s headline inflation slowed to 1.7% YoY, marking the lowest rate since late 2024 and undershooting the ECB’s 2 % target. Core inflation also eased to about 2.2%, indicating softer underlying price pressures outside energy/food. This backdrop reinforces expectations that the ECB will hold interest rates steady in the near term.

Corporate Deals: → Texas Instruments (mcap $203bn) to acquire Texas-based wireless-technology company Silicon Labs (mcap $6.6bn) for $7.5bn ($231/share cash, including debt) in a semiconductor consolidation play targeting home, healthcare, and industrial IoT applications. The deal promises EPS accretion in year one and $450 million annual synergies within three years. Silicon shares jumped 49% today and is 55% higher YTD.

→ German consumer goods company Henkel AG (mcap €32bn) will acquire Netherlands-based speciality coatings firm Stahl for €2.1bn (including debt) from Wendel, expanding its adhesives business into high-growth coatings for home, healthcare, and industrial applications. The deal follows Henkel’s ATP Adhesive purchase, targeting €1.2bn net proceeds for Wendel and accelerated growth in adhesive technologies.

→ Zurich Insurance’s sweetened $11bn bid (up to 1,335 GBp/share) has won over UK insurer Beazley, whose board is now open to recommending it after prior rejections over undervaluation.

→ In IPOs, Connecticut-based hair loss company Veradermics priced its upsized IPO at $17 per share, raising $256mn, implying a fully diluted valuation of about $596mn. Shares more than doubled to $37.75 on their NYSE debut.

Day Ahead:

Monetary Policy → ECB (unch at 2.15% exp), BoE (unch at 3.75% exp), Banxico (unch at 7% exp). Data → €-zone retail sales, Germany factory orders. Earnings → Amazon, Shell, Unilever, BNP, BBVA, Conoco P, Linde, BMS.

See you tomorrow.

Copyright © 2025 Succinct.

All rights reserved. This publication contains proprietary content and is intended solely for the recipient’s personal use. Disclaimer: Our service is for informational purposes only and does not constitute personal financial advice.