Wed 4 Mar: After the Bell

Stocks Rise Despite Escalating Middle East Conflict; Rate-Cut Bets Fade:

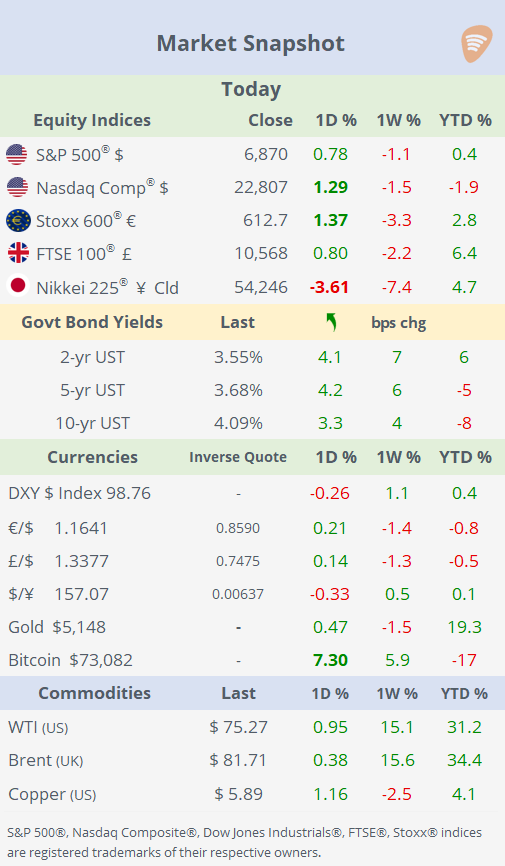

ℹ️Today’s Performance tables.

Good evening,

Equities rebounded on Wednesday as risk appetite improved amid reports that Iran may have indirectly signalled openness to talks, lifting US and European stocks (not Asia) despite ongoing volatility. However, officials remain sceptical, oil prices stayed elevated, and markets trimmed expectations for a June Fed rate cut (to a 33% prob) as inflation risks resurfaced.

Meanwhile, the Middle East conflict continued to escalate on the ground, with fresh strikes, Iran’s naval losses in the Indian Ocean, and the Strait of Hormuz blockage trapping around a fifth of global oil and LNG supply, keeping geopolitics firmly at the centre of the market narrative.

Korea’s KOSPI index (-12%) underperformed sharply as the oil shock hit a major energy-importing economy, triggering heavy foreign selling and forced unwinds in large tech names, amplifying losses well beyond other markets.

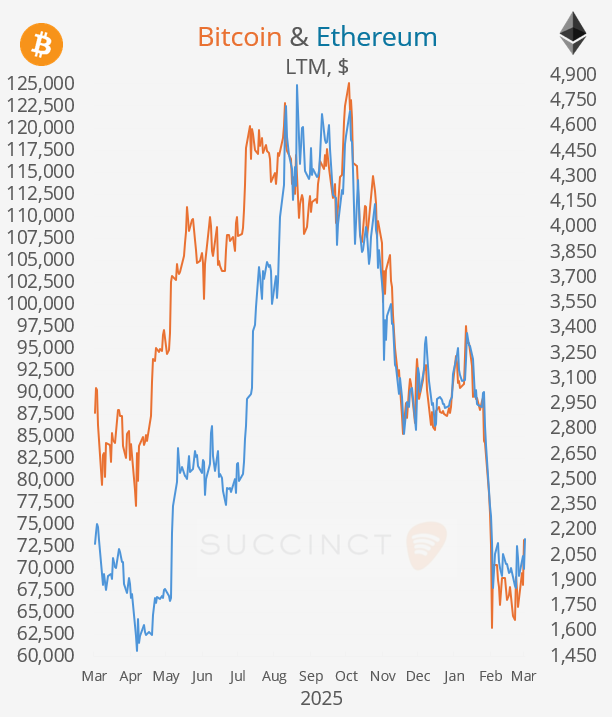

Bitcoin jumped 8% today to a four-week high, boosted by news that Kraken Financial, Kraken Exchange’s banking arm, became the first crypto bank granted a Fed “master account,” giving direct access to Fedwire for payment settlements. This milestone signals growing integration of digital assets into the US financial system.

After the close, Broadcom’s quarterly revenue guidance topped estimates, with the stock trading sideways in after-hours.

Economics: → The Fed’s Beige Book showed a mixed US economic picture in February, with modest growth in seven districts offset by flat or declining activity in five, as hiring remained stagnant and tariffs raised business costs. Consumer spending edged up slightly, but uncertainty, price sensitivity, and winter storms restrained retail activity.

→ US (ADP) private sector employment rose by +63,000 jobs in February, surpassing consensus (50k) and marking the largest monthly gain since mid‑2025, with strength led by education and health services and payrolls beating forecasts. Wage growth remains solid (~+4.5% YoY), suggesting some stabilisation in the labour market ahead of the official government jobs report, though gains are still concentrated in select sectors.

→ The US ISM Services PMI surged to 56.1 in February, hitting a 3½-year high and signalling robust expansion in services activity, new orders, and employment. However, the S&P Global Services PMI (a different survey method) showed a softer pace (~51.7), indicating growth remains modest in some segments.

→ €-zone producer prices (PPI) rebounded in January, rising +0.7% MoM and signalling renewed upstream inflation pressures after previous declines. However, the YoY change remained negative at ‑2.1% for the sixth consecutive month, underscoring persistent disinflation in wholesale prices despite short-term monthly gains.

Central Banks: → Today’s Fed commentary split between dovish voices arguing geopolitical risks shouldn’t derail eventual rate cuts, and hawkish or cautious officials stressing inflation is still too high and favouring holding rates steady longer.

Cleveland Fed’s Hammack said it’s too early to gauge the impact of the Iran conflict on inflation and supported holding interest rates steady for an extended period rather than cutting them soon. Fed Governor Miran stated that ongoing risks shouldn’t delay planned rate cuts this year, and he still sees further easing as appropriate despite recent oil price moves. Kansas City’s Schmid emphasised inflation remains “too hot” and indicated no urgency for the Fed to ease policy, reinforcing a more hawkish tone versus cuts.

Corporate Deals: Market turmoil limited deal announcements, with few transactions coming to market.

→ In private markets, Neura Robotics, a German startup building AI-powered collaborative and humanoid robots, is raising €1bn in a round backed by Tether (the crypto stablecoin company), targeting a valuation of ~€4bn. The company focuses on cognitive and industrial robots, including the 4NE1 humanoid, for manufacturing, logistics, and human-interactive applications. (BBG)

→ In IPO’s, PhonePe, the Indian digital payments firm backed by Walmart, is moving ahead with IPO plans in India. According to sources, PhonePe is targeting a valuation of roughly $10bn, implying proceeds of about $1bn. As part of the listing, Walmart is expected to trim its stake, while Microsoft and Tiger Global are set to exit. The offering comes as PhonePe continues to dominate India’s payments ecosystem, having processed nearly half of all UPI transactions in January, underscoring its scale and strategic relevance ahead of the IPO. (Reuters)

Day Ahead: Data → US initial jobless claims; €-zone retail sales; Korea inflation. Earnings → Costco, Merck, Deutsche Post, Kroger, Gap.

See you tomorrow.

Copyright © 2026 Succinct.

All rights reserved. This publication contains proprietary content and is intended solely for the recipient’s personal use. Disclaimer: Our service is for informational purposes only and does not constitute personal financial advice.