Wed 8 Apr: After the Bell

Relief Rally: Ceasefire Sparks Global Risk-On Surge

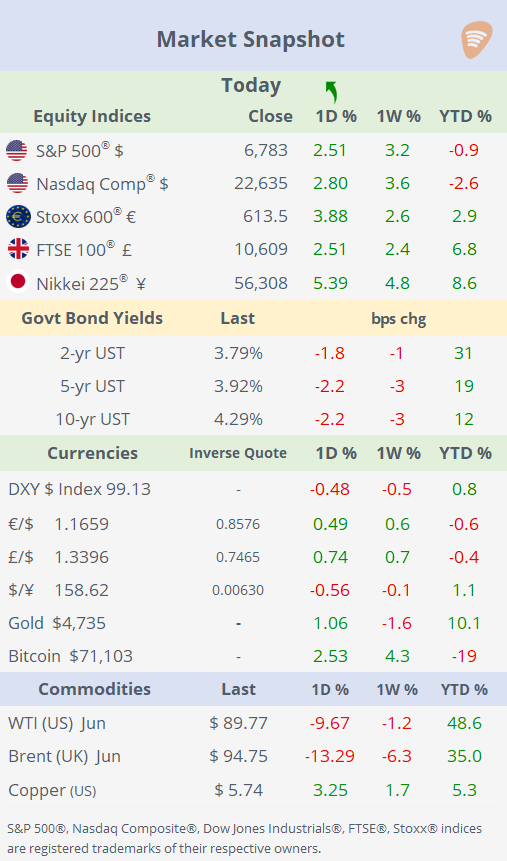

📈 Today’s performance tables.

Good evening,

A dramatic shift in the geopolitical backdrop triggered a full-blown risk-on reversal across global markets. Washington’s last-minute ceasefire agreement with Iran, secured just an hour before the deadline set by Trump, sparked a powerful rally in risk assets. The S&P 500 surged nearly 3% to a one-month high, while European equities jumped 5%. Crude oil collapsed 13% in what marks one of the sharpest single-day declines in years, as immediate supply disruption fears eased.

The move extended across asset classes. The $ weakened notably, with the DXY Index falling to 99, its lowest level in four weeks, against broad strength in the €, £, and Swiss franc. At the same time, Treasuries traded firmer, reinforcing the synchronised nature of the move: lower oil, weaker dollar, and higher equities, a classic unwind of geopolitical risk premium.

Notably, markets moved decisively ahead of confirmation. Investors did not wait for evidence that the ceasefire would hold or for shipping flows through the Strait of Hormuz to normalise. Instead, positioning rapidly shifted toward de-escalation, driving what can best be described as a relief rally across risk assets, even as missiles and drones reportedly continued to be exchanged in the region.

However, cracks began to emerge into the close. Reports of ceasefire violations and continued hostilities introduced fresh uncertainty, with the US preparing direct talks led by Vice President Vance. Oil prices rebounded ~2% after the close following the historic drop, highlighting how fragile sentiment remains. For now, markets are trading on the hope of de-escalation, but with headline risk still firmly in control.

Economics: → FOMC Minutes reinforce a cautious, hawkish stance, with policymakers flagging persistent inflation risks and signalling limited urgency to cut rates. Updated projections show a higher inflation path into 2026, implying policy may need to stay restrictive for longer, with any shift toward easing remaining strictly data dependent. Futures imply a ~98% chance for no rate change by the Fed at its next meeting in 20 days and the following in mid-June.

→ €-zone retail sales slipped 0.2% MoM after a modest prior gain, reinforcing a pattern of choppy and fragile consumer demand, with weakness typically driven by non-food and fuel categories. Despite a still positive +1.7% YoY print, the data suggests only a gradual, uneven recovery in consumption, consistent with subdued confidence and soft underlying growth momentum.

→ The Reserve Bank of India kept rates unchanged at 5.25%, maintaining a neutral, “wait-and-watch” stance as policymakers assess the impact of the Iran conflict on inflation and growth. Officials warned that energy-driven inflation risks are rising, with CPI seen at ~4.6% and growth at ~6.9%, while disruptions could pressure activity, keeping policy on hold unless risks materially shift.

Deals: → In private markets, PE firm General Atlantic is acquiring San Diego-based Team Services Holding, a non-medical home care company, for ~$3bn (incl. debt), implying 10x EBITDA and highlighting continued private equity appetite for stable, cash-generative healthcare services. The deal underscores a rotation toward traditional healthcare assets, less exposed to AI disruption, while targeting growth in home-care demand, particularly driven by aging demographics and cost-efficient care models.

→ A potential £10bn sale of a controlling stake in privately owned Associated British Ports, which handles 25% of UK seaborne trade, has attracted interest from major infrastructure investors including KKR, Global Infrastructure Partners and DP World. The stake is being sold by Canadian pension funds (CPPIB and OMERS), highlighting strong demand for large-scale, resilient infrastructure assets with stable cash flows, and setting up a potentially competitive bidding.

→ In IPOs, The Metals Royalty Company (TMCR), which acquires and manages metals and mineral royalties and streams to support mining sector growth in North America, completed a direct listing on Nasdaq. The stock began trading at ~$12 per share and closed at $14, implying a market cap of $770mn.

Day Ahead:

Data → US PCE inflation, personal spending & income; Mexico inflation; Germany trade and industrial production.

Earnings → Progressive Corp.

Copyright © 2026 Succinct.

All rights reserved. This publication contains proprietary content and is intended solely for the recipient’s personal use. Disclaimer: Our service is for informational purposes only and does not constitute personal financial advice.