Wed 8 Oct: After the Bell

🎙️📄+ Market Data -> Equities rally, FOMC minutes, ¥ drops, Palladium, Cocoa, First Brands ...

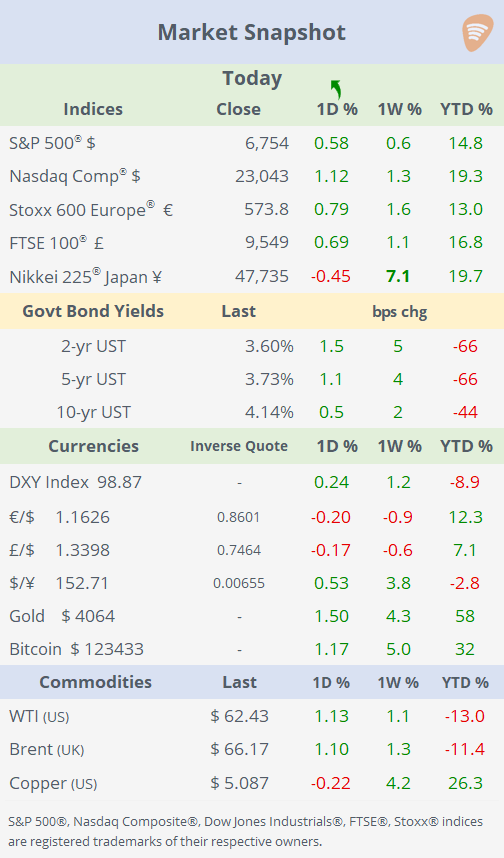

See the ‘Market Data’ post for tables & charts.↗

Good evening,

Stocks on Wall Street and Europe rallied on Wednesday, driven by optimism from the Federal Reserve minutes’ dovish tone, boosting risk appetite across equities. The S&P 500 and Nasdaq are again at all-time highs. The tech sector gained on renewed momentum in AI chip stocks due to the recent mega-deals, also fueling investor enthusiasm. Despite the ongoing government shutdown, market confidence remained resilient, showing little impact.

The $ index advanced mainly on the back of a weaker ¥. This combination of Fed dovishness and tech sector strength shaped today’s positive market sentiment.

Japan’s stock market reached record highs this week following the appointment of a new prime minister, with the Nikkei 225 index accumulating a 20% gain this year. The rally is attributed to expectations of increased fiscal stimulus and a continuation of loose monetary policies. The ¥ weakened to a seven-month low against the dollar, dropping to 153, as markets anticipate sustained dovish policies.

Commodities: A notable mover today was Palladium, with a 9% rally to $1,500 as investors seek alternative trades to gold and growing market concerns over potential sanctions on Russian exports.

Cocoa futures slumped to a 20-month low ($5,960/ton in New York and $4,260/ton in London), driven by improved harvest prospects in West Africa and higher payments to farmers. The reversal ends the dramatic rally that pushed prices above $12,000 last December, with mounting supply and weak chocolate demand accelerating the decline.

US soybean farmers are under pressure as China hasn’t booked any purchases in months, raising fears of a “bloodbath.” China, which accounted for over half of last year’s $24.5bn in soybean exports, has increasingly turned to Brazil and Argentina, forcing American farmers to seek alternative markets. The Trump administration has already missed a self-imposed deadline this week to announce aid for farmers, and ongoing gridlock on Capitol Hill suggests delays may continue. Soybean futures have traded range-bound this year and are little changed YTD.

Special Situations: First Brands Group, the Ohio-based privately owned auto parts supplier, filed for Chapter 11 bankruptcy at the end of September, citing over $10bn in liabilities, including $6bn in debt and significant off-balance-sheet financing tied to customer invoices and inventory. The event has led to substantial financial exposure for major financial institutions. UBS’s O’Connor hedge fund unit (acquired by Cantor), reported $500mn in exposure, representing 30% of one fund, and Jefferies’ Point Bonita Capital with $715mn at risk.

Central Banks: The FOMC’s minutes from the Fed’s September meeting, released today, reveal a significant policy shift towards further easing. The Fed implemented its first interest rate cut of the year, reducing the target rate by a quarter point to a range of 4.00%–4.25%. This decision was influenced by a softening labour market and growing downside risks to employment, despite inflation remaining above the 2% goal. The minutes also indicated that several officials favoured a more aggressive rate cut, with some dissenting members advocating for a half-point reduction.

Data: Germany’s industrial production fell sharply in August, dropping 4.3% MoM versus an expected 1.0% decline. On an annual basis, output is down 7.3%, reflecting ongoing weakness in the sector and a slowdown in manufacturing demand. The automotive sector was particularly impacted, experiencing an 18.5% monthly decline, largely due to annual factory closures and model changeovers.

With the US employment report delayed by the government shutdown, alternative data is drawing attention. Wall Street estimates, including Carlyle Group, suggest only 17k jobs were added in September, down from 22k in August. Bank of America reports a 10% rise in jobless claims YoY, signalling a cooling labour market.

Corporate Deals: SoftBank agreed to acquire ABB’s robotics division for $5.4bn, expanding its push into AI-driven automation. The deal supports Softbank’s strategy to build a comprehensive AI ecosystem spanning robotics, chips, and data infrastructure. Shares in the Swiss Swedish industrial technology group are 20% higher this year to an all-time high and a market cap of $134bn.

IPOs: Swedish home-security group Verisure priced its IPO at €13.25, for a total value of €13.7bn and was multiple times oversubscribed. The listing on Nasdaq Stockholm raised roughly €3.2bn, marking Europe’s largest IPO since 2022, with shares surging 20% on debut.

Day ahead: Germany balance of trade; Mexico and Brazil inflation; Pepsico and Delta Air earnings; US jobless claims (suspended).

See you tomorrow.

Copyright © 2025 Succinct.

All rights reserved. This publication contains proprietary content and is intended solely for the recipient’s personal use. Disclaimer: Our service is for informational purposes only and does not constitute personal financial advice.